- | Academic & Student Programs Academic & Student Programs

- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

The Deduction of State and Local Taxes from Federal Income Taxes

Removing the federal tax deduction for state and local taxes would make taxes more equitable throughout the nation, as both high-tax and low-tax states are treated equally by the federal government. It may also provide an efficiency boost for states and localities, as they abandon some services that could be better provided by private companies. The removal of this deduction would also allow federal marginal tax rates to be cut across the board, providing a secondary boost to the economy while still remaining revenue-neutral at the federal level.

Taxpayers who itemize their deductions are allowed to deduct state and local taxes from their federal taxable income. This deduction is limited to either income or sales taxes, but not both. Personal property taxes, such as local taxes on housing and real estate, can also be deducted. The main benefit of this deduction is to provide some tax relief to taxpayers living in states with higher taxes, since they have less disposable income. However, this benefit also points to the main cost of the deduction: it subsidizes higher taxes and spending at the local level, since taxpayers in those states will not feel the full burden of the taxes. Instead, the burden of these taxes is in some sense “exported” to taxpayers in other states, since federal tax rates must be higher than otherwise to fund the same level of federal spending.

When discussing taxation in the United States, it is important to consider all levels of taxation rather than just focusing on one at a time, such as federal income taxes, because these tax levels affect each other. One way in which these taxes interact is found in the federal income tax code, whereby taxpayers who itemize deductions are able to deduct a variety of state and local taxes when calculating taxable income. In most years it is one of the five largest tax expenditures in the individual income tax, and it is thus one of the largest “tax expenditures” as defined by government agencies, such as the Office of Management and Budget.1 OMB estimates that in fiscal year 2012, this deduction reduced federal tax revenue by about $45 billion, and this amount will roughly double over the next five years. As a result, this deduction has had a large impact upon the overall tax system of the nation at all levels of government, which warrants further analysis of its overall desirability.

Two Concerns For Equity

The distribution of the benefits of this tax expenditure, as well as the costs of removing it, can be thought of in two ways. First, there is the question of which taxpayers within the distribution of income benefit the most. According to estimates by the Joint Committee on Taxation for 2012, almost 95 percent of the benefits of this deduction go those earning over $75,000 per year, and over half (55 percent) of the benefits are for those earning over $200,000. The average deduction for those in the over $200,000 income group is over $5,000, while it is only about $250 for those in the $50,000 to $75,000 group (around the national median).2 These averages only include those taxpayers that claimed the deduction, which is only 27 percent of all taxpayers since most do not itemize their deductions.

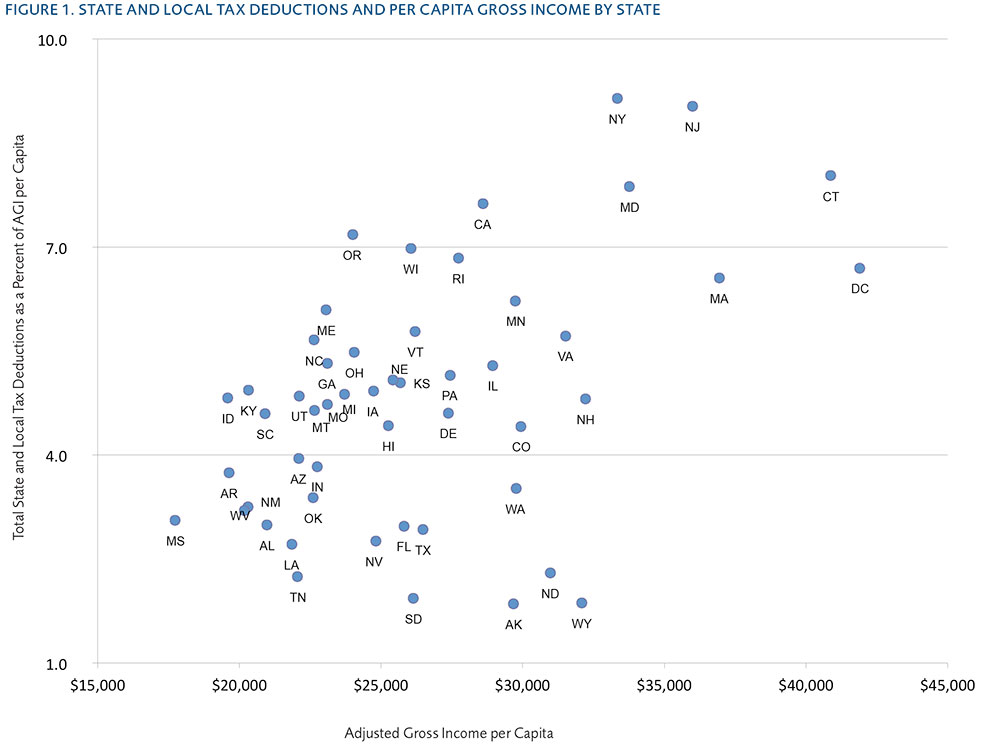

Second, there is the distribution of benefits across the 50 states, based on how high taxes are in each state. States with higher taxes will have more filers claiming this deduction, and therefore the deduction will also be a larger share of the state’s income. These high-tax states also tend to be high-income states, implying that there is a transfer from low-income to high-income states through this deduction. By looking at the total deductions in this category as a percent of adjusted gross income, we can see that there is wide variation across the states. The states with the lowest state and local tax deductions (Alaska, Wyoming, South Dakota) claim deductions amounting to less than two percent of their adjusted gross income, while the highest tax states (New York and New Jersey) claim over nine percent of their adjusted gross income. The figure below plots the correlation between the total deduction for state and local taxes and per capita adjusted gross income for 2010 for all 50 states and DC.3

Redistribution Or Offset For Higher Taxes?

During the 1985 tax debate, NYU law professors Brookes Billman and Noel Cunningham offered an economic justification for the deduction: state and local taxes reduce an individual’s income and ability to pay federal taxes, which should then be considered by the federal tax code.4 After all, if federal taxes should be based on an individual’s ability to pay, then local taxes could reasonably be considered as reducing one’s ability to pay federal taxes.

Economist Bruce Bartlett took a contrary position to Billman and Cunningham, arguing that this deduction is a subsidy to high-tax states from low-tax states, and high-tax states tend to have higher per capita incomes. He also found that, in general, the deduction is associated with higher state and local taxes because the federal government is paying a portion of these taxes, with most estimates suggesting state and local taxes are about 13 to 14 percent higher.5 In this case, more services may be provided publicly, even if it is more efficient to provide them privately. This deduction also influences the types of taxes that state and local governments use, biasing them toward choosing taxes that are deductible rather than those that are most efficient.6 More recent estimates confirm that state and local spending “could fall in the absence of deductibility,” indicating that the deduction does indeed increase government spending.7

Furthermore, the ability-to-pay reasoning of Billman and Cunningham overlooks where state and local taxes go, since taxes are not only collected, but spent. Unless one views all government spending as complete waste, it is a reasonable assumption that the local taxes are providing some services to those that pay them (though likely not equal to the full value of taxes paid in many cases). Thus, local taxes don’t reduce an individual’s willingness to pay by the full amount of the tax, or possibly even at all. The local taxes an individual pays are returned to the individual as local government services, minus the costs and wastes associated with government provision of services.

For example, in cities where garbage collection is provided by the local government, the property or sales taxes that fund this service are deductible. For cities where garbage collection is provided privately, the fees paid to the garbage company are not tax deductible. But from an economic perspective, these two situations are identical and should be treated the same in the tax code. The current tax code gives preference to city-provided garbage collection, which potentially violates both equity and efficiency. The tax code also biases municipalities towards providing services, such as garbage collection, even though it may be more efficient for these services to be provided privately.

Tax Rates And Macroeconomics Effects

Eliminating the deduction for state and local taxes will likely lead to increased macroeconomic activity by removing the economic distortions listed above. It will also potentially lead to more federal tax revenue, though this depends on how individuals react to what would be, in effect, a tax increase. A better policy would be to simultaneously decrease tax rates at the same time that this deduction is eliminated, generating additional economic activity without increasing the amount of revenue concentrated at the federal government.

Estimating the economic and tax-revenue effects is a difficult matter. Two recent studies by the Tax Foundation attempt to examine the effects of removing the deduction for state and local income, sales, and property taxes. These estimates should not be taken as definitive point estimates, but as indicative of the direction of the effects. For the state and local income and sales tax deduction, they estimate that eliminating the deduction combined with an across-the-board cut in individual income tax rates by 5.8 percent (i.e., the 10 percent rate would drop to 9.42 percent) would result in an increase in total employment by around 300,000 jobs.8 They found similar effects for the property tax deduction, though this would also require a decrease in business property taxes because “capital (even owner-occupied housing) is quite sensitive to taxes.” 9

Conclusion

Removing the federal tax deduction for state and local taxes would make taxes more equitable throughout the nation, as both high-tax and low-tax states are treated equally by the federal government. It may also provide an efficiency boost for states and localities, as they abandon some services that could be better provided by private companies. The removal of this deduction would also allow federal marginal tax rates to be cut across the board, providing a secondary boost to the economy while still remaining revenue-neutral at the federal level.

Notes

- For a discussion of the largest individual and corporate tax expenditures, see Jeremy Horpedahl and Brandon Pizzola, “A Trillion Little Subsidies: The Economic Impact of Tax Expenditures in the Federal Income Tax Code” (Mercatus Research, Mercatus Center at George Mason University, Arlington, VA, October 25, 2012).

- See Table 3 of Joint Committee on Taxation, Estimates of Federal Tax Expenditures for Fiscal Years 2012–2017 (Washington, DC, February 1, 2013), JCS-1-13. The JCT estimates do not provide any further details on the about $200,000 group, but due to AMT and phase-outs of deductions, it is likely that the benefits are not flowing to taxpayers with extremely high incomes.

- Deduction totals include property taxes and either income or sales taxes. Tax data from Internal Revenue Service, SOI Tax Stats—Historical Table 2, updated April 23, 2013, http://www.irs.gov/uac /SOI-Tax-Stats---Historic-Table-2.

- Brookes D. Billman Jr. and Noel B. Cunningham, “Nonbusiness State and Local Taxes: The Case for Deductibility,” Tax Notes 28 (September 2, 1985): 1105–1120.

- Bruce Bartlett, “The Case for Eliminating Deductibility of State and Local Taxes,” Tax Notes 28 (September 2, 1985): 1121–25.

- Martin Feldstein and Gilbert Metcalf, “The Effect of Federal Tax Deductibility on State and Local Taxes and Spending,” Journal of Political Economy (1987): 710–36.

- Gilbert Metcalf, “Assessing the Federal Deduction for State and Local Tax Payments,” National Tax Journal 64 (June 2011): 565–590.

- Michael Schuyler and Stephen J. Entin, “Case Study #4: The Deduction of State and Local Income Taxes or General Sales Taxes,” Tax Foundation Fiscal Fact, no. 382 (August 2013).

- Stephen J. Entin and Michael Schuyler, “Case Study #2: Property Tax Deduction for Owner-Occupied Housing,” Tax Foundation Fiscal Fact, no. 380 (July 2013).