- | Regulation Regulation

- | Data Visualizations Data Visualizations

- |

Did Deregulation Cause the Financial Crisis? Examining a Common Justification for Dodd-Frank

In Dodd-Frank: What it Does and Why it’s Flawed, we used the RegData methodology to estimate that Dodd-Frank will cause a 26 percent increase in financial regulatory restrictions. Policymakers should reexamine the presumption that Dodd-Frank’s substantial regulatory restrictions are necessary to offset previous deregulation of the financial services sector. On net, RegData shows that no such deregulation occurred. In fact, the financial sector was increasingly regulated over the decade leading up to the financial crisis.

Three years ago the Dodd-Frank Wall Street Reform and Consumer Protection Act was signed into law. Deregulation of the financial services sector in the years leading up to the 2008 crisis was—and still is—used to justify Dodd-Frank’s substantial regulatory burdens. But financial regulation did not decrease in the decade leading up to the financial crisis—it increased.

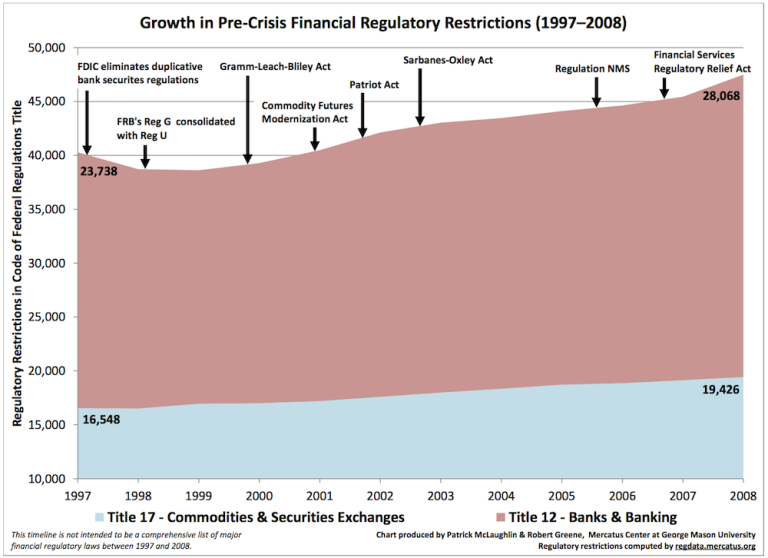

Using the Mercatus Center at George Mason University’s RegData, we find that between 1997 and 2008 the number of financial regulatory restrictions in the Code of Federal Regulations (CFR) rose from approximately 40,286 restrictions to 47,494—an increase of 17.9 percent. Regulatory restrictions in Title 12 of the CFR—which regulates banking—increased 18.2 percent while the number of restrictions in Title 17—which regulates commodity futures and securities markets—increased 17.4 percent.

RegData measures regulatory restrictions by counting the number of restrictive words and phrases—such as “may not,” “must,” “shall,” “prohibited,” and “required”—in each title of the CFR. Developed by Patrick A. McLaughlin and Omar Al-Ubaydli, RegData is computer-based and thus only able to calculate regulatory restrictions for 1997 and subsequent years because electronic copies of the complete, annual CFR are publicly available from the Government Printing Office for only that time period.

Total regulatory restrictions pertaining to the financial services sector grew every year between 1999 and 2008, increasing 23 percent during this time. The Patriot Act, the Sarbanes-Oxley Act, and Regulation NMS all contributed to this growth. The repeal of parts of the Glass-Steagall Act via the Gramm-Leach-Bliley Act did not result in noticeable deregulation of the financial services sector. Nor did the Commodity Futures Modernization Act facilitate overall financial deregulation. Not even the Financial Services Regulatory Relief Act of 2006, legislation intended to decrease regulatory burdens on the financial industry, reversed the ever-growing burden of regulatory restrictions faced by the financial services sector in the years leading up to the financial crisis.

Net decreases for Title 12 regulatory restrictions between 1997 and 1999 largely reflect an effort to streamline regulatory text. Only the FDIC portion (volume 4) of Title 12 experienced a significant decrease in pages between 1997 and 1998, and it was almost entirely isolated within 12 C.F.R. § 335, which was shortened from 136 to 7 pages in an effort to streamline FDIC regulations with pertinent SEC Securities Exchange Act regulations. Similarly, the comparatively small decrease in overall regulatory restrictions in Title 12 between 1998 and 1999 is in large part attributable to the Federal Reserve’s 1999 consolidation of Regulation G—which pertained to nonbanks’ extension of leverage for the purpose of purchasing certain securities—with Regulation U, which was revised to be applicable to both banks’ and nonbanks’ extension of leverage. Without this consolidation, Title 12 pages would have increased between 1998 and 1999. Neither of these episodes had any relation whatsoever to Gramm-Leach-Bliley or the Commodity Futures Modernization Act.

As we show in this analysis, financial regulatory restrictions increased 17.9 percent in the years leading up to the crisis. Without the streamlining efforts of the late 1990s—which reduced duplicative regulatory text and were unrelated to the acts of Congress typically blamed for alleged deregulation—this figure would likely be even higher. In Dodd-Frank: What it Does and Why it’s Flawed, we used the RegData methodology to estimate that Dodd-Frank will cause a 26 percent increase in financial regulatory restrictions. Policymakers should reexamine the presumption that Dodd-Frank’s substantial regulatory restrictions are necessary to offset previous deregulation of the financial services sector. On net, RegData shows that no such deregulation occurred. In fact, the financial sector was increasingly regulated over the decade leading up to the financial crisis.

Related Content

- | Regulation Regulation

- | Working Papers Working Papers

RegData

- | Financial Markets Financial Markets

- | Books Books

Dodd-Frank: What It Does and Why It's Flawed

- | Financial Markets Financial Markets

- | Expert Commentary Expert Commentary