- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

The Economic Situation, October 2012

This special Mercatus Center edition of my Economic Situation report focuses on what I call the stumbling U.S. economy. In the report, I seek to explain how and why the economy is performing so poorly. I do this by assessing some of the economy’s major features. The first assessment involves an examination of the economy’s uneven pulse beat, best seen in GDP growth data. I then turn to state unemployment and state GDP growth data and present another picture of uneven growth. After discussing federal budgets and deficits, I turn to labor markets and then to an assessment of the Federal Reserve Board’s efforts to stimulate the economy using quantitative easing. I conclude this special report with a brief review of what has happened to income distribution and a short summary of what I expect we will see across the rest of 2012 and in 2013.

October 2012

• The stumbling U.S. economy lacks a prosperity foundation

• What has happened to the great American job machine?

• Will quantitative easing help?

• What has happened to household income?

• What lies ahead?

The Stumbling U.S. Economy Lacks a Prosperity Foundation

Introduction

This special Mercatus Center edition of my Economic Situation report focuses on what I call the stumbling U.S. economy. In the report, I seek to explain how and why the economy is performing so poorly. I do this by assessing some of the economy’s major features. The first assessment involves an examination of the economy’s uneven pulse beat, best seen in GDP growth data. I then turn to state unemployment and state GDP growth data and present another picture of uneven growth. After discussing federal budgets and deficits, I turn to labor markets and then to an assessment of the Federal Reserve Board’s efforts to stimulate the economy using quantitative easing. I conclude this special report with a brief review of what has happened to income distribution and a short summary of what I expect we will see across the rest of 2012 and in 2013.

The economy’s uneven pulse

The latest revisions of GDP data tell us that the U.S. economy is barely operating in positive growth territory. Real GDP growth for 2Q2012 was revised down to 1.3% from an earlier 1.7% estimate. The margin between growth and recession is thin. There is little room to absorb shocks that may come from the ongoing European recession, possible trade disturbances with China, the approaching fiscal and regulatory cliffs, and unexpected natural disasters that have a way of coming at the worst possible times.

Ours is a stumbling economy with little in the way of knee pads to cushion a fall.

When we rake through the data, we find little in the way of what I call a general prosperity foundation for economic growth. Instead, economic growth is being lifted by specialized energy production—coal, gas, ethanol, oil—some parts of manufacturing, especially in the auto sector, and export sales. Bruised and beaten by the housing market collapse, construction—by far the weakest sector—hardly has a pulse. Things are looking up a bit, but construction is years away from what might be called “normal” levels of activity. The U.S. economy will not be back in its running shoes until the housing sector is finally cleared of past overinvestment, bad debt, and bankruptcies.

From the standpoint of individual Americans, how the economy is doing depends on where you live, what you do for a living, and how badly your region or industry suffered in the Great Recession. There are vast differences in economic well-being to be found across the 50 states.

How the states are faring

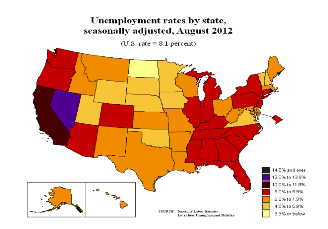

We can see this in a number of ways. Consider the next chart, which shows levels of unemployment by state for August 2012 and is the most recent data map available from the Bureau of Labor Statistics. Things are brightest in the Dakotas, Iowa, Wyoming, and other western states that produce energy and hard grains. The Mississippi River forms one dividing line that separates stronger from weaker states. The Rocky Mountains form another. To the east, we find older manufacturing regions with correspondingly higher unemployment rates. Michigan’s burgeoning auto industry is an exception, as is West Virginia’s coal economy and Virginia’s government research economy. To the west are declining states that experienced huge construction activity setbacks in conjunction with the deflated housing bubble. These states lack a specialized recovery sector.

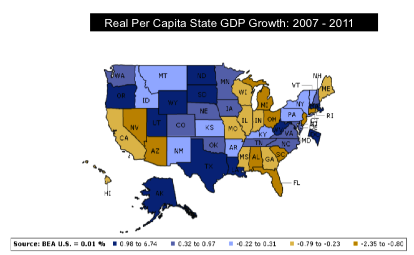

The next chart shows state GDP growth across 2007–2011.We see evidence of specialized prosperity, not general wealth creation.

Once again, prosperity is found in the west, weakness along the coasts.

While a prosperity foundation that could be formed by multiple expanding sectors is lacking, immediate prospects are not bright. Europe’s decline as well as uncertainties regarding taxes, regulation, and policies for dealing with the looming deficit are taking their toll.

What do GDP data tell us?

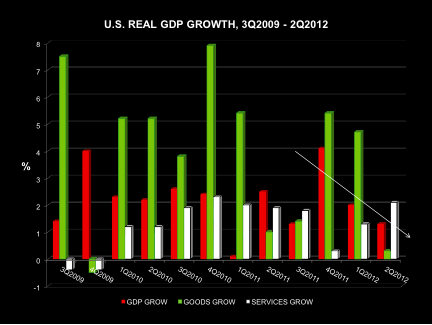

The next chart shows GDP growth data. The data begin with 3Q2009 when real GDP growth for the nation first turned positive following the Great Recession. The data extend to 2Q2012. Along with real GDP growth, shown in red, I include growth in goods production (green) and services (white), which are two major economic sectors. The goods sector includes manufacturing, construction, and public utilities.

I call attention first to the red GDP growth bar. GDP growth in 3Q2009 was pushed into positive territory by the Cash for Clunkers program that led to early purchases of more than 600,000 vehicles. Clunkers lifted 3Q2009 goods production, which then fell dramatically in 4Q2009. Across 2010, GDP growth leveled out at about 2%. Note that goods production—manufacturing—was the driver. As 2011 arrived, Europe’s problems, Japan’s March 2011 natural disaster, and U.S. deficit uncertainties caused goods production and services to weaken. This took a toll on overall GDP growth. We saw recovery in the last part of 2011, but then a second European hit arrives. The data for 2012 were decidedly weaker. When I drew a trend line through the GDP or goods growth data for the last three quarters, the line pointed south. The services sector growth looks much better.

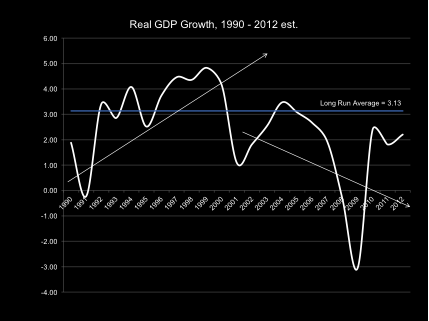

Annual rates of GDP growth for the years 1990–2011 are shown in the next chart. The data describe two very different growth paths that seem to be separated by 9/11. The pre-9/11 path is strong and rising; the post-9/11 path is weak and falling. We can see that GDP growth exceeded the long run 3.13% average just once after 9/11. Based on expectations for the rest of 2012, economic growth will remain in the cellar.

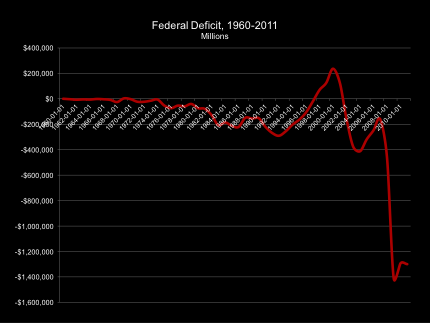

We are indeed traveling on a bumpy GDP growth path. It has been a rough trip since 9/11 placed the nation on a troubled road. The road has seen a costly war with losses of human beings—the ultimate resource—disruptions of families, community life and work. While taking on terrorism and building enhanced homeland security, the nation also expanded government services generally and then was hit by the financial collapse and recession that followed. As a result, we placed a huge amount on the nation’s credit card. The results are seen in the next chart.

What about the federal budget?

The federal spending profile is not very pretty. With the exception of the years 1998–2001, our federal government expenditures have exceeded revenues for every year since 1969. Following 9/11, the nation’s surplus turned to a deficit. Then, the Great Recession and continued expansion of federal programs pulled the plug on deficit spending. There seemed to be no bottom.

Today, we face a perplexing situation. There is no congressional agreement on comprehensive budget reform. Large legislated tax increases are on the books for January 2013. And costly environmental regulations have been put on hold until next year. The pending hit is large enough to tilt the economy into a 2013–2014 recession. At the same time, the nation lacks a prosperity foundation for lifting GDP growth nationwide. Yes, new wealth is currently being created, let’s not forget that, but at a weak pace.

While riding a bumpy expansion path, the slow economy cannot generate meaningful employment growth. But there is more to the story than just suggesting that higher growth rates could magically solve the nation’s unemployment problems.

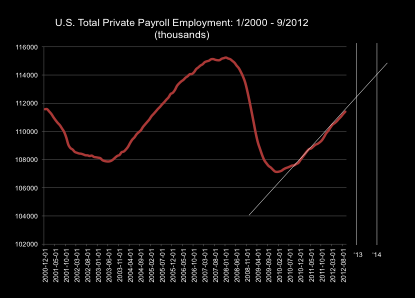

What Has Happened to the Great American Job Machine?

National employment data seen in the accompanying chart tell us the post-recession economy is healing. Here, we see total private payroll employment for the U.S. economy January 2000–September 2012. We observe the pre-recession employment peak in January 2008. We then see rapid job losses, the bottoming out in January 2009, and the recovery that continues. The white trend line in the data indicates that if the current pace of job growth continues, we will again achieve peak 2008 employment levels around mid-2014. But we know that when employment recovers the unemployment rate will be higher than it was in 2007, simply because there will be a much larger labor force in 2014 than we had in 2008.

How do we get more jobs?

Jobs! This is the topic of the day, yesterday, and tomorrow. How do we get more jobs? In a few words, real jobs with a real future have to be generated by the real economy, not by temporary government actions that provide support but lack a prosperity foundation.

Real jobs develop when people in markets decide on their own to buy more goods, build more schools and houses, or invest in more plants. By comparison, stimulus programs generate temporary jobs with an uncertain future. With luck, stimulus jobs may just happen to become real jobs. But making this work encounters a tremendous knowledge problem. The record on designing just the right fiscal policy to achieve lasting employment gains is poor. The U.S. and world economies are just too massive, too complicated, and filled with too much uncertainty for a government planner’s dreams to become a main street reality. The brightest and best Washington policymakers can simply not get a fix on the real economy, how it is performing, which sectors might be targeted for special treatment, and which ones not targeted. And if they could, there is still a political decision-making process to engage before policy, no matter how brilliant, becomes fact.

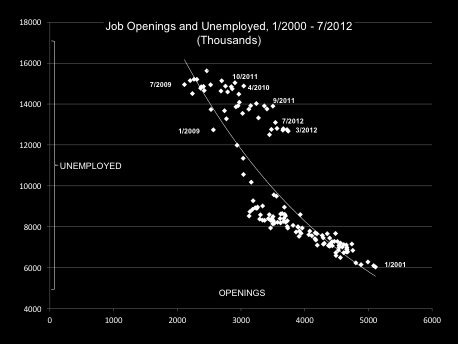

As it turns out, the economy is generating job openings that are not being filled. There is a serious mismatch in the kinds of jobs that are opening and the locations and talents of the unemployed who are seeking jobs. We saw indirect evidence of this in the August 2012 unemployment map shown earlier in the report. For example, North Dakota had a 3% unemployment rate in August. Jobs go begging there. Nevada’s unemployment rate was 12.1%. Prospects are bleak there. We get a national view of the mismatch problem in the next chart. Here we see a mapping of the number of jobs being opened nationally each month and the number of people counted as unemployed. Normally, when the number of new job openings is high and rising, the number of people still looking for work falls. The general shape of the data confirms this.

I have given dates for some of the observations in the chart to help identify a time dimension found in the data. But consider the array of 2011–2012 observations in the chart’s upper sector. Here we see recent observations where openings are at a higher level but the number of unemployed remains stubbornly high.

Why the mismatch?

There are at least three explanations for the mismatch. First, if job openings in the new economy call for experienced workers with higher skills and educational attainment and the unemployed are primarily unskilled workers with low educational attainment, then jobs go unfilled. A second explanation relates to the difficult housing market. Job openings occurring in another state may require the job searcher to relocate. Selling a home anywhere has been difficult. It is especially difficult in high unemployment regions. The third explanation has to do with expanding benefits for people who are searching for jobs. With extended unemployment benefits, people can search a bit longer, maybe enroll in a community college, and hold out for a better job. All three explanations may be at play, but we know more about the skill mismatch and the tough housing market than the effects of extended unemployment benefits.

For example, we know that the unemployment rate in September 2012 for people over 25 with bachelor degrees was 4.1% nationwide. For people over age twenty-five who lack a high school diploma, the rate is 11.3%. The data tell us there is a mismatch. One part of the mismatch comes from the weak construction sector that is barely breathing and the many construction workers who lack the educational credentials to fill jobs in manufacturing and services. I note that in January 2008 there were 7.4 million employed in construction. In September 2012, the number employed in the sector stood at 5.5 million. Some 1.9 million construction workers have been displaced since 2008. Interestingly enough, the number employed has just hit bottom and is finally rising a bit. We will not see a return to a low overall unemployment and newly prosperous economy until the construction sector is revived.

The data tell us there are structural and geographic unemployment problems that cannot easily be resolved by way of top-down stimulus spending. People are not putty in high speed vehicles that can instantly be reshaped and shipped to fill the needs of a particular stimulus project or expanding sector.

Will Quantitative Easing Help?

Throughout the massive financial crisis and Great Recession, the Federal Reserve has taken unprecedented actions in an avowed attempt to protect the integrity of the nation’s banking system, encourage investment, and improve economic growth. In conjunction with the Federal Deposit Insurance Corporation and the Treasury, the Fed has cooperated in consolidating failing banks and protecting the financial assets of the American public.

Doing these things is not just about softening blows to the banking system. It is about protecting the system that creates money that, in turn, feeds our economic system.

New money enters the economy when banks make loans. Money disappears when borrowers pay off their loans. Both money and bank capital disappear when borrowers go bankrupt. Bankruptcies can destroy families and impose huge hardships. The epidemic of bankruptcies since 2008 caused the money supply to contract, housing prices to fall, banks to fail, and economic growth to stall.

The Fed has a number of tools to use in an effort to offset these problems. The Fed can influence interest rates by buying and selling previously issued U.S. government bonds. It can make it easier for banks to borrow from the Fed and change the amount of money banks must hold back in reserves. And the Fed can simply create money out of thin air. Using “thin air” journal entries, the Fed creates new money and uses that money either to buy newly issued bonds from the U.S. Treasury or to buy bonds held by banks and other institutions. Any combination of these actions puts new money into the banking system. This is called printing new money or quantitative easing (QE).

Having pretty well exhausted the use of the other tools, and with interest rates that borrowing banks pay each other floating close to zero, the Fed has now engaged in three QE episodes, with the third one just getting started. QE-1 took place November 2008–March 2010 when the Fed purchased $1.7 trillion in Treasury bonds, mortgage backed securities, and federal agency debt. QE-2 operated November 2010–June 2011 and involved the purchase of $600 billion from the U.S. Treasury. QE-3 was announced in September and will involve the continuing purchase of $40 billion monthly in mortgage-backed securities, with no deadline imposed but with the goal of improving the employment situation.

The Fed doesn’t really work for the president of the United States. The Fed resides outside of government; it is an independent body that generates its own budget and then some. Its annual surplus is paid to the U.S. Treasury.

QE actions can initially reduce interest rates on private debt and juice up the stock market. This has happened. But for QE to increase bank lending, the newly created money has to make its way out of the banking system and into the economy. Banks that previously had bonds on the shelf may now have excess reserves with the Fed—more reserves than required—that can be turned into loans. While holding those reserves with the Fed, banks earn interest. But holding reserves doesn’t increase economic activity.

So here’s the question: Have excess reserves been converted into loans?

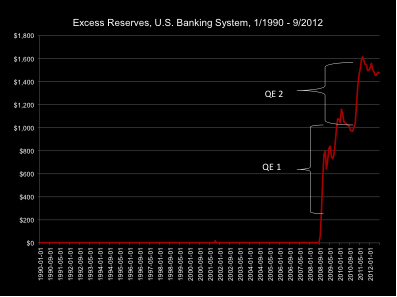

We can determine this by examining the level of excess reserves held by all banks taken together. The data may reveal the results of the QE programs. If excess reserves held in the system rise and stay high, then we can infer that lending will not have expanded. If reserves rise and then fall, then lending will have increased.

Data on excess reserve for the entire banking system are shown in the next chart. As can be seen, in normal times, excess reserves stay close to zero. Banks are lending as much as their reserves allow; they have lots of creditworthy borrowers. As your eyes travel along the almost zero line, you will come to 9/11. There you see a small blip, which at the time was a sizable increase in Fed-provided reserves to cushion the effects of the attack. But notice what has happened with the financial collapse. Excess reserves have skyrocketed to levels never seen before. And notice what happened with QE-1 and QE-2. Excess reserves rose with QE-1 a lot but by less than the amount of money printed. The reserve jump with QE-2 is about equal to the amount of funds injected. Bank lending was apparently enhanced during the QE-1 period. In the most recent months, excess reserves are falling, which is another indication that banks are lending. This is a sign that creditworthy borrowers are showing up in bank lobbies. And that is an indication that Q-3 going forward may help.

The key, of course, is creditworthy borrowers.

All this may sound almost rosy. But as with most prescribed remedies, there are potential side effects that we should consider. What is the QE risk? Look at the level of excess reserves just waiting to be converted into loans. If QE-3 were to become suddenly effective, loans would shoot up, money would run out the door of banks, investment would rise, new housing starts would expand, and retail sales would look like perpetual pre-Christmas shopping.

And all this excitement would be accompanied by galloping inflation—unless a very agile Fed is able to reverse the engines and back money out of the system.

That is the risk. And the Fed is very much aware of it.

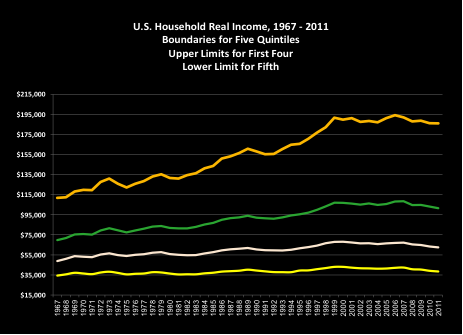

What Has Happened to Household Income?

Using U.S. Census bureau data, I have prepared a chart that shows U.S. household income for the years 1967–2011. The numbers, adjusted for inflation, are for earned income, which does not include transfer and welfare payments. The data are arrayed in quintiles with the upper limits of household income shown for the first four quintiles and the lower limit for the top quintile. As the next chart tells us, the stumbling U.S. economy ceased to produce meaningful wealth increases across U.S. households after 1996. But during the golden days of 1990–1996, America’s highest income group cheered all the way to the bank. Prior to this, significant income gains were generated for the top-two income quintiles and modest gains were registered for the third quintile. But little movement occurred in the two lowest quintiles. If we call the third quintile the middle class, the data tell us the middle group saw gains until about 1999, but, like the other quintiles, lost ground after that.

What Might Lie Ahead?

I close out this special Mercatus Center edition of the Economic Situation report with all best wishes and an outlook summary for 2012–2013.

Related Content

- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

The Economic Situation, September 2012

- | Regulation Regulation

- | Policy Briefs Policy Briefs

The Economic Situation, June 2012

- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

The Economic Situation