- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

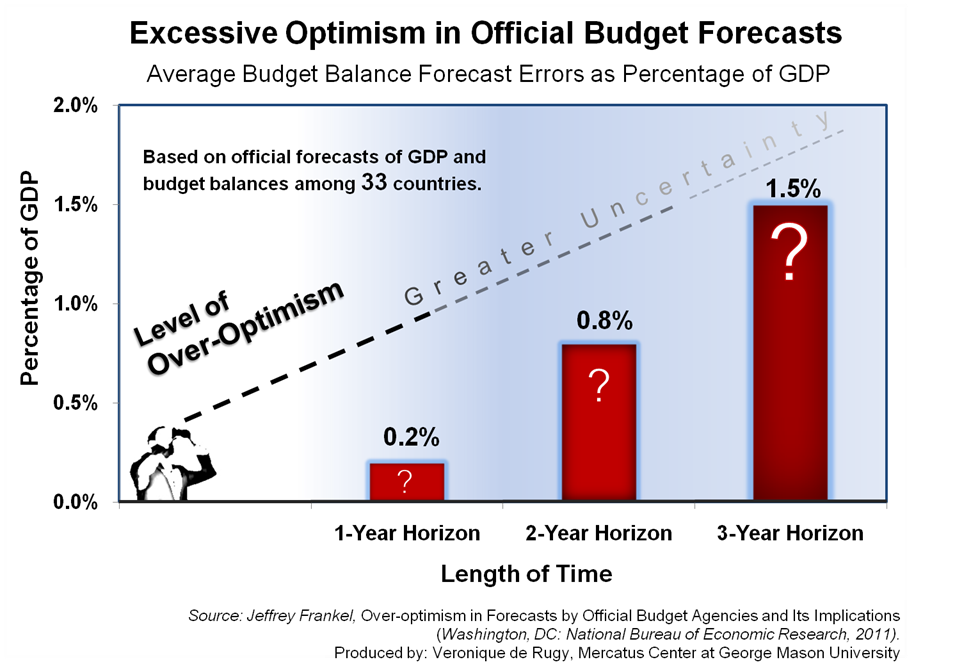

Excessive Optimism in Official Budget Forecasts

Average Budget Balance Forecast Errors as Percentage of GDP

This week's chart illustrates the bias toward over-optimism in official forecasts of GDP and budget balances among 33 countries.

This week, Mercatus Center Senior Research Fellow Veronique de Rugy draws insights from a recent study by Harvard economist Jeffrey Frankel of the National Bureau of Economic Research (NBER), to chart findings of the bias toward over-optimism in official forecasts of GDP and budget balances among 33 countries. The chart depicts the magnitude of forecast errors (as a percentage of GDP) increasing as the time horizon increases. This upward trend suggests that over-optimism thrives when genuine uncertainty is higher; which is often the normal state of affairs for most of the government agencies in the budget forecasting process.

Overly optimistic economic assumptions for estimates of economic growth lead to over-optimism in budget estimates. As evidence, Frankel’s paper suggeststhat the average upward bias in the official forecast of the budget balance, relative to the realized balance, is 0.2 percent of GDP at the one-year horizon, 0.8 percent at the two-year horizon, and 1.5 percent at the three-year horizon. However, the United States tends to be even more over-optimistic than other countries. Franklin explains: “The U.S. forecasts have substantial positive biases around 3% of GDP at the three-year horizon (approximately equal to their actual deficit on average; in other words, on average they repeatedly forecast a disappearance of their deficits that never came).”

Unsurprisingly, optimism bias is more pronounced during boom times, or times of economic prosperity. But Frankel also found that optimism is present during busts, too. He writes, “Evidently official forecasters […] over-estimate the permanence of the booms and the transitoriness of the busts.”

This is unfortunate as adoption of realistic economic growth outlook can play an important role in achieving successful fiscal adjustments. For instance, it was an important factor in the unanticipated budget surplus of the 1990s in America. According to the International Monetary Fund, “when formulating the five-year budget plan, the Clinton Administration adopted a realistic growth outlook, projecting real GDP growth below 3 percent and gradually declining.” Soon after, the U.S. experienced a budgetary surplus from 1998 to 2001. Similarly, Frankel argues that U.S. budget forecasts made by the White House in 2001 and subsequent years is a case where “unrealistic forecasts were plausibly a major reason for the failure of the U.S. to take advantage of the opportunity to save during the 2002-07 expansion.”

Considering the implications of such forecasting errors; particularly on how over-optimism contributes to excessive deficits and the perpetuation of political opportunism, improvements to the overall system would be important. However, it is at least as important to realize that it is not forecast that matters, rather it is how these forecasts are used to achieve political goals. As such, any attempts by forecasters to remind readers that they should be highly skeptical of forecasts is a good idea.

Veronique de Rugy discusses the fallibility of government agency projections at The Hill.