- | Housing Housing

- | Working Papers Working Papers

- |

Modeling State Credit Risks in Illinois and Indiana

The author uses an open-source budget-simulation model to evaluate Illinois’s credit risk and to compare it to that of Indiana, a neighboring state generally believed to have better fiscal management. Based on a review of the history and theory of state credit performance, he assumes that a state will default if the aggregate of its interest and pension costs reaches 30 percent of total revenues. His analysis finds that neither state will reach the critical threshold in the next few years under any reasonable economic scenario, suggesting no material default risk.

1. Modeling Illinois’s Credit

Is Illinois in serious jeopardy of insolvency? The state has the lowest credit ratings in the nation, and its long-term general-obligation bonds yield 1 percent more than those issued by the most highly rated states, reflecting a market perception of significant credit risk. As a result, Illinois taxpayers pay tens of millions of dollars in additional interest charges—costs that could be avoided if the state were perceived to be a safe investment.

In this study, I estimate the risk of an Illinois bond default by performing a multiyear fiscal simulation. I also model a neighboring state, Indiana, which is perceived by rating agencies and the credit markets to be a much less risky issuer. The simulation analysis produces estimates of bond-default probability that can be used to determine whether the extra interest costs borne by Illinois taxpayers properly compensate bondholders for the incremental risk they are shouldering. In addition to modeling bond-default risk, the fiscal-simulation model also enables us to consider the impact of future interest and retirement costs on each state’s ability to support its commitments to health, human services, education, and other programmatic spending priorities.

The simulation model I use in this analysis requires a default point: a fiscal threshold at which the state can be expected to become insolvent. Selecting a default point requires us to review the history of US state credit. After establishing this default point, I then consider a number of other key issues that will affect Illinois’s long-term solvency. Specifically, I measure the state’s existing debt burden and consider the likely trajectory of key expenditure areas, including pensions, other post-employment benefits (OPEB), education, and health care. Next, I explain the modeling framework and assumptions, and I conclude by presenting the model results and their implications.

The model results suggest that Illinois state bonds carry very little credit risk and that Indiana’s obligations are even less risky. While Illinois’s fiscal policies are likely to have negative effects on future state residents and implications for other public policies, they are not sufficiently dangerous to worry bondholders.

II. A Brief History of Illinois Debt

Neither Illinois nor Indiana has a spotless credit record—both defaulted in the early 1840s. A lot has changed in the last 170 years, so it may be reasonable to ignore these historical payment failures. On the other hand, Reinhart and Rogoff (2009) demonstrate the benefits of considering very long time series when studying sovereign-debt crises. Because there has been only one default by a sovereign member of the Organisation of Economic Co-operation and Development since World War II and no default by a US state since that time, it is essential to consider the more distant past to see what a future default might look like.

Illinois took on substantial debt in 1836 and 1837 to finance the construction of a canal connecting the Illinois River to Lake Michigan, and to capitalize two state banks. Illinois bonds all carried interest rates of 6 percent. The high rate (by contemporary standards) reflected the speculative nature of these bonds. When the bonds were issued, the state did not generate sufficient tax revenue to service them. Buyers were effectively relying on the canal project to raise property values and thereby generate enough property-tax revenue for the state to make interest and principal payments.

A severe financial panic in 1837 was followed by a nationwide economic downturn in the late 1830s and early 1840s. Illinois continued issuing bonds to finance the canal, cover the state’s operating expenses, and even fund interest payments on previously issued debt. By September 1841, the state had $13.6 million in bonds outstanding, all carrying a rate of 6 percent (US Congress, 1843). The approximately $800,000 in interest costs exceeded state revenues in 1841 by a factor of more than four (Krenkel, 1958). In December 1841, Illinois bonds were trading at less than 30 cents on the dollar. Lacking a market for new bonds and the revenue to service existing issues, the state defaulted in January 1842 (United States Magazine and Democratic Review, 1842).

Tax revenues eventually increased, especially after the opening of the canal in 1848. In 1857, the state fully emerged from default, and by 1880 Illinois’s state debt was fully repaid (Moody’s, 1934). Illinois remained debt-free until after World War I. Between 1918 and 1923, voters approved a series of bond issues totaling $235 million to fund highway construction, build the Illinois Waterway, and pay a bonus to war veterans. In 1932 and 1936, a further $50 million was approved to support emergency relief (Illinois state comptroller, various years).

By the end of World War II only about $100 million of these bonds remained outstanding. In 1947 voters approved $385 million to pay bonuses to World War II veterans (Moody’s, 1948). Little borrowing occurred during the next two decades, and by 1970 the state’s general-obligation debt load of $266 million remained below its 1947 level—even in nominal terms.

It was only after 1970 that the state’s debt burden began its relentless climb to today’s levels (US Census Bureau, various years). In 1970, voters authorized $750 million in antipollution bonds (Chicago Daily Defender, 1971) and ratified a new state constitution that allowed the legislature to unilaterally approve new bond issues. Under the previous constitution, general-obligation bonds required voter approval. In 1971, Republican Governor Richard Ogilvie proposed $900 million in additional bonds to fund transportation projects (Wall Street Journal, 1971).

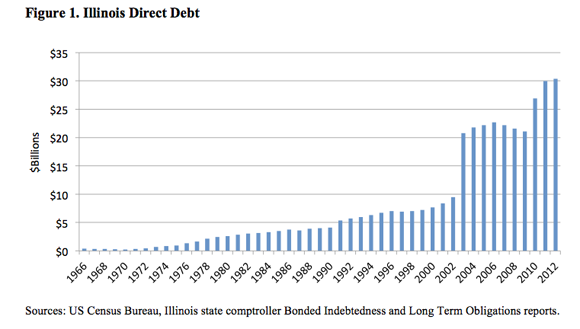

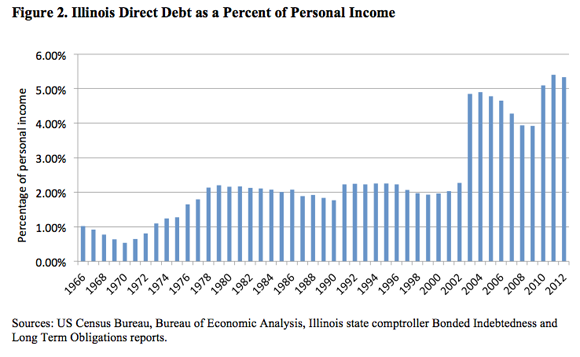

As shown in figure 1, since 1970 Illinois’s direct debt (debt that is directly serviced from state tax revenues) has risen by a factor of over 100 in nominal dollars to its current level of roughly $30 billion. The escalation is dramatic even if changes in population, real income, and prices are taken into account. Figure 2 shows the ratio of direct debt to personal income—an economic aggregate that contains most components of GDP. After bottoming at 0.54 percent in 1970, this ratio has climbed to 5.34 percent in 2012.

III. Defaults in Other States and Analogous Subsovereign Entities

Like Illinois, Indiana also took on substantial debt ahead of the 1837 panic. In addition to canal building and bank capitalization, the state borrowed to support railroad construction (US Congress, 1843). As was the case with Illinois, Indiana’s interest costs exceeded annual revenues (Wallis, 2005).

The Illinois and Indiana defaults were part of a wave of state insolvencies that followed the Panic of 1837 (Wallis, 2005). A second wave of state-bond defaults occurred in the former Confederate states during Reconstruction (Joffe, 2012a).

As reported by Fons, Randazzo, and Joffe (2011), the most recent US state-bond defaults occurred in 1933. In that year, Louisiana failed to make payments on certain bond issues due to the temporary closure of Hibernia Bank, where funds earmarked for debt-service payments had been deposited. This default, which was cured within three months, occurred before the inception

of federal deposit insurance, and would most likely not have happened had the FDIC been in place. Also, in late 1932 and early 1933 South Carolina was unable to redeem maturing bonds for cash and instead provided bondholders new market-rate bonds with later maturities. There is no evidence that the state missed interest payments. While this case is a default in bond-market terms, it did not result in a material loss of value to bondholders.

More serious was the case of Arkansas, which failed to make interest payments on March 1, 1933, and remained in a state of partial default until 1941, when the Reconstruction Finance Corporation—a federal agency created during the Depression—bought the state’s debts at par. Ultimately, bondholders received all promised interest and principal, but on a substantially delayed basis. According to the contemporary Moody’s bond manual (1934), Arkansas bonds traded as low as 40 cents on the dollar shortly after the initial default, representing a substantial loss to any bondholder that needed to liquidate at the time.

Over the last 140 years, the Arkansas situation is the only case in which a state defaulted on interest payments owed to individual investors as a result of a fiscal crisis. It is thus the most relevant default case available, and it merits further study. On the eve of the Arkansas default, interest costs accounted for roughly 30 percent of state revenues—far above the level for any other state. Other Depression-era government-bond defaults in the Anglophone world—including those of Australia, New Zealand, New South Wales (an Australian state) and Alberta (Canada)—were also accompanied by interest-to-revenue ratios of 30 percent or more (Joffe, 2012b).

Discussions about the risk of sovereign-debt crises often revolve around the debt-to- GDP ratio. In the 1930s, GDP was not measured. Economists have provided retrospective estimates of GDP at the national level, but not for individual states. The Bureau of Economic Analysis (2006) has produced gross state product (GSP) estimates back only as far as 1963. Consequently, it is not possible to provide a precise estimate of Arkansas’s debt-to-GSP ratio at the time of its default.

While an estimate of Arkansas’s debt-to-GSP ratio in 1933 would be interesting, it would not—in my opinion—provide the best measure of maximum debt sustainability. The use of economic output as a denominator fails to capture differences between governments’ ability to harvest revenues from their respective tax bases. Modern governments in advanced economies have been able to collect greater proportions of GDP in the form of taxes than governments that preside over large numbers of subsistence farmers—either historically or in developing countries today. Further, subsovereign governments like those of the US states typically have less revenue- collecting power than national governments. Consequently, the maximum sustainable debt-to- GDP ratio for states is likely to be lower than it is for sovereign powers.

Debt-to-GDP ratios also fail to capture differences in interest rates. Postwar Britain and modern Japan both sustained very high debt-to-GDP ratios because they faced very low interest rates. The ratio of interest expenses to total revenue incorporates both the level of interest rates and the government’s ability to collect revenue from its tax base. Consequently, it is a more consistent measure of debt sustainability across time, and it takes into account levels of economic development and the government’s degree of sovereignty (i.e., whether it is a nation, province, state, or locality).

The interest-to-revenue ratio also correctly captures the public-choice aspect of government default. The payment or nonpayment of debt-service obligations is not a macroeconomic aggregate; it is a decision made by a relatively small group of government officials. Critics of government debt modeling correctly observe that default is a political decision, but the choices of individual actors—including political leaders—can be and have been modeled.[1]

In this case, the choice is between the embarrassment and loss of bond-market access triggered by default and the crowding out of programmatic spending arising from continued debt service. During a time of budgetary stress, the options are to cut payments to bondholders or beneficiaries. The dynamics of this choice were captured in a 1931 speech by New South Wales premier Jack Lang when he announced the Australian state’s default on a £700,000 interest payment:

Parliament in New South Wales was faced with an extremely awkward problem. It was committed to pay to oversea [sic] bondholders £700,000. The Government itself had not the money. It was informed, however, that this amount would be made available for shipment overseas if the Government needed it. Having in mind the reiterated statement that every £ of credit consumed by the Government meant a £ less for circulation among the primary and secondary industries, the Government was faced with a most difficult problem. If we took the £700,000 which the bank offered us, it meant that £700,000 worth of credit would have to be withdrawn from the primary and secondary industries of New South Wales. Default faced us on either hand. We could default, if we chose, to the farming community by withdrawing £700,000 from it, or we could default to our oversea creditors. Having to choose between our own people and those beyond our shores, we decided that the default should not be to our own citizens. (Sydney Morning Herald, 1931)