- | Academic & Student Programs Academic & Student Programs

- | Regulation Regulation

- | Policy Briefs Policy Briefs

- |

The Pitfalls of Regulating Consumer Credit

Government regulators proposing restrictions on specific forms of consumer credit all too often ignore the reality of how and why consumers use credit. They also ignore lenders’ legitimate reasons for pricing their services as they do; consumers’ legitimate reasons for choosing the financing options they do; the risks consumers face when credit offerings are made unavailable to them; and the many consumers who use the particular forms of consumer credit responsibly and effectively.

Government regulators proposing restrictions on specific forms of consumer credit all too often ignore the reality of how and why consumers use credit. They also ignore lenders’ legitimate reasons for pricing their services as they do; consumers’ legitimate reasons for choosing the financing options they do; the risks consumers face when credit offerings are made unavailable to them; and the many consumers who use the particular forms of consumer credit responsibly and effectively.

As a result, new laws and regulations on consumer credit have unintended consequences that frequently harm the very people they are meant to help by making credit more expensive and harder to obtain; by inducing lenders to reprice non-interest-rate terms and reduce transparency; and by forcing consumers to substitute less-preferred types of credit. The restrictions also harm individuals and families that don’t use any form of consumer credit by inducing banks to increase fees on bank accounts, ATM transactions, and other services. Low-income individuals and families are particularly harmed by these fees and may even be forced out of the traditional banking system altogether as simple checking accounts become less affordable. Additionally, regulations on some forms of consumer credit may drive consumers into other, perhaps even more problematic, forms of credit.

Regulators must be mindful not to restrict consumers’ access to credit nor to increase the cost of credit by well-intentioned but misguided laws and regulations.

HOW AND WHY CONSUMERS USE CREDIT

Consumers use credit for the same basic purposes as businesses: to make capital investments that return value over time and to smooth temporary mismatches between income and expenses.

First, consumers use credit to make capital improvements, such as in consumer durables. A consumer may finance a car purchase, which returns value over time by reducing travel times, easing the physical burden of walking long distances, and replacing the need to pay for bus or cab fare. Similarly, purchasing a washing machine generates convenience and cost-savings as consumers do laundry at home rather than at laundromats.

Second, consumers use credit in order to smooth temporary budget shocks, such as an unexpected cut in income or a large, unexpected expense. Unavailability of credit can result in non-payment of bills or bounced checks, which can put consumers at risk of potentially disastrous financial penalties, termination of bank accounts, eviction, discontinuation of utilities or medical treatment, or other problems. In such cases, the question foremost on consumers’ minds is not whether the expenditure will be made but how it can be financed.

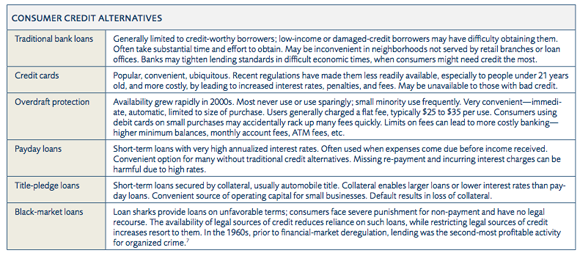

Those in need of credit have many potential options, beginning with informal, personal sources of credit (e.g., loans from family and friends or advances from their employers) and mainstream solutions such as credit cards and traditional bank loans. But informal credit is often unavailable, especially in amounts necessary to meet urgent expenditures. Most people simply don’t have rich friends and relatives from whom they can obtain substantial loans on short notice. And main- stream credit such as credit cards may not be available either, especially to low-income borrowers and those with damaged credit. For these less-affluent or less-financially-secure individuals and households, what happens when a paycheck is expected on Friday but rent is due on the preceding Tuesday?

Those with convenient access to traditional retail banking may have checking accounts with overdraft protection, which is a form of consumer credit that has become more common over the past twenty years. A person writing a check on Tuesday from an account with insufficient funds is effectively being loaned the amount of the overdraft until he or she can add sufficient funds back into the account on Friday. Over- draft protection avoids bounced checks and their associated monetary fees, embarrassment, and distrust. Overdraft protection is also very convenient, since it works automatically. The bank, however, charges a fee (usually a flat fee regard- less of overdraft amount) for each use of the overdraft protection service. With increasing use of debit cards for minor everyday purchases, horror stories have arisen of hundreds of dollars in overdraft fees stemming from a handful of small purchases, say of $2 coffees and the like, and such seemingly disproportionate charges have led regulators to scrutinize overdraft protection fees for possible regulatory oversight. But empirical research indicates that, while these stories of inadvertent triggering of overdraft fees do occur, they are not representative of regular users of overdraft protection, who often have limited credit options and use overdraft protection knowingly in order to balance their financial affairs.[1]

Payday loans—short-term unsecured loans intended to be repaid upon the receipt of expected income within a pay period—may legitimately be the most attractive option, due to their convenience, reliability, and availability on short notice. Most payday loan customers do not have credit cards or would exceed their allowable credit limits if they used credit cards. Payday loans therefore fill an important gap in the supply of financial services to the poor. These loans do have high effective interest rates, but research shows those high prices can be explained by the high costs of originating and servicing many small loans and their high risk of default.[2]

Title pledge lending, usually auto title pledge lending, offers a third type of credit for many borrowers. Unlike overdraft protection and payday loans, both of which require consumers to have bank accounts, many auto title loan customers are “unbanked”—they lack traditional bank accounts—and thus turn to auto title lending instead. Other users of title loans include independent small businesses (such as a handyman or landscaping company) that use their trucks or vans as col- lateral to obtain short-term operating capital during a job. Finally, some auto title customers are people who have relatively high income but bad credit for some reason and thus are unable to obtain a credit card or open a bank account.[3]

Although these various alternative lending products appear to be expensive, as noted above, consumers choose rationally in deciding whether to use these consumer-credit offerings and in deciding which particular offering to use. Indeed, the existence of these and other types of credit offerings gives consumers more flexibility because they can choose their source of credit based on the factors that matter most to them: interest rates, repayment periods, and origination and other fees are important but not the sole factors consumers consider. Convenience and accessibility are important factors that many regulators fail to appreciate. Payday lending offices may provide the only source of short-term credit avail- able to residents of neighborhoods lacking traditional bank branches. In addition, many of those who use alternative financial products have had negative experiences with credit cards or banks in the past, having fallen subject to expensive penalties and other charges. As a result, these consumers often value the simplicity and pricing-transparency of alter- native credit products.

So consumer-credit decisions are about tradeoffs, where consumers balance availability, convenience, cost, legality, risk, and any other relevant considerations. Not surprisingly, different consumers, having different financial circumstances and needs, opt for different sources of credit, and their credit preferences may change over time as their circumstances change. And the competition among the many alternatives generally improves the terms of all of them.

UNINTENDED CONSEQUENCES OF REGULATING CONSUMER CREDIT

Well-intentioned legislators and regulators assume that restricting particular forms of credit will lead to fewer bad financial outcomes. But this is misguided and can lead to worse, not better, outcomes. Restrictions on particular types of consumer credit don’t necessarily induce consumers to refrain from unnecessary purchases or to avoid bad out- comes. Consumers resort to these financing options because they have pressing needs. So repressing one form of consumer credit will often only lead to a shift to other new or existing forms of consumer credit offered on less favorable terms for consumers. Restrictions on payday lenders might simply turn them into title lenders, as they seek to make up for caps on fees and interest rates by demanding collateral to reduce losses in the event of default, or push consumers to online payday lenders, which often charge higher rates than brick-and-mortar payday lenders. The ad hoc regulatory program of restricting disapproved forms of consumer credit thus has a whack-a- mole nature to it; limiting one form simply spawns a new one that avoids existing regulations.

But worse than channeling some consumers into less-preferred forms of credit is the possibility of killing off credit for others. Approximately nine million households, or 7.7 percent of all the households in the United States, do not have a traditional bank account.[4] Restricting access to particular forms of credit that seem foolish to well-paid bureaucrats can actually leave those unbanked individuals and house- holds without any access to credit at all. Caps on payday-loan interest rates can induce lenders to be pickier in choosing to whom they will lend, resulting in fewer people being able to obtain credit. They may also induce lenders to require larger principal amounts or to lengthen the period of the loan, thus increasing the cost to the borrower potentially above what the borrower can afford, leaving all borrowers worse off and some entirely unable to obtain credit.

Well-meaning limitations on banks’ credit-financing fees can actually increase the number of unbanked households. If banks can’t charge as much for overdraft protection, they must try to maintain profitability by charging more on other services such as ATM withdrawals; adding or increasing fees on basic checking accounts; increasing minimum-balance requirements and increasing fees on low balances; charging more for checks; adding charges for in-person and ATM services; etc. Indeed, in the wake of new regulations on overdraft protection (in the Federal Reserve’s amendments to Regulation E) and price controls on debit card interchange fees (in the Durbin Amendment to the Dodd-Frank legislation), the percentage of retail bank accounts eligible for free checking dropped precipitously,[5] as did the percentage of consumers with a checking account.[6] The resulting cost hikes on basic accounts and services can price poor individuals and families, including those who never used overdraft protection, right out of the market. Those not entirely priced out of the banking system are still harmed by the increased fees.

Banks may also simply close branches to trim costs in response to the regulations. The New York Times reports that in 2010, "for the first time in 15 years, more bank branches closed than opened in the United States" -- and it's the poor who bear the brunt of the inconvenience when this happens. [8]

Worse still, the poor who are left without access to legal sources of consumer credit may land in the arms of loan sharks and other black-market operators, or they may resort to financing their expenditures via illegal, dangerous, or risky endeavors. The absence of legal sources of credit can thus be extremely harmful.

CONCLUSION

Government actors seeking to regulate consumer finance offerings no doubt intend to help the individuals and families who use them, but the economic reality of consumers’ desire for credit often results in unintended consequences from new regulations that leave consumers worse off, not better. We cannot simply ignore or wish away consumers’ need for credit, and we ought not to ignore the majority of consumers who use these products responsibly. Politicians and bureaucrats need to understand the important and legitimate roles various forms of consumer credit play in the financial lives of consumers, both poor and non-poor, and to acknowledge the appropriate role that fees, interest rates, and other terms of credit play in regulating its availability.

ENDNOTES

- For a discussion of how consumers use overdraft protection, including references to empirical research, see Todd J. Zywicki, “The Economics and Regulation of Bank Overdraft Protection” (Working Paper No. 11-41, Mercatus Center at George Mason University, 2011).

- For a more in-depth discussion of payday lending, including discussion of term pricing, see Todd J. Zywicki, “The Case Against New Restrictions on Payday Lending” (Working Paper No. 09-28, Mercatus Center at George Mason University, 2009).

- Todd J. Zywicki and Gabriel Lucjan Okolski, “Potential Restrictions on Title Lending,” (Mercatus on Policy, no. 62, Mercatus Center at George Mason University, 2009).

- FDIC Survey of Unbanked and Underbanked Households, http://www. fdic.gov/householdsurvey/. The Federal Reserve’s 2008 Survey of Con- sumer Payment Choice reported that 6 percent of those in the study did not have bank accounts. See Scott Schuh and Joanna Stavins, “How Consumers Pay: Adoption and Use of Payments” (Federal Reserve Bank of Boston Consumer Payments Research Center Working Paper No. 12-2, December 12, 2011), 4. In addition, according to the FDIC Survey, approximately 21 million households, or 17.9 percent of households, are “underbanked,” meaning that even though they have a checking or sav- ings account, they also use alternative financial services such as money orders, check-cashers, payday loans, rent-to-own, or pawn shops at least once or twice a year or have refunded anticipation loans at least once in the past five years.

- It fell from 76 percent in 2009 to 65 percent in 2010, and then to 45 percent in 2011. See David S. Evans, Robert E. Litan, and Richard Schmalensee, “Economic Analysis of the Effects of the Federal Reserve Board’s Proposed Debit Card Interchange Fee Regulations on Consum- ers and Small Businesses” (Federal Reserve Consumer Impact Study, February 22, 2011), http://www.federalreserve.gov/SECRS/2011/ March/20110308/R-1404/R-1404_030811_69120_621655419027_1. pdf; and Claes Bell, Abracadabra: Free Checking Disappears, BANKRATE.COM (September 26, 2011), http://www.bankrate.com/ finance/checking/abracadabra-free-checking-disappears.aspx.

- From 92 percent in 2010 to 88 percent in 2011. Javelin Research & Strat- egy, Javelin Study Finds Prepaid Cards Lure Underbanked and Gen Y Consumers (San Francisco, CA: Javelin Research & Strategy, April 11, 2012), http://finance.yahoo.com/news/javelin-study-finds-prepaid- cards-164300454.html.

- U.S. Congress, House Government Operations, Legal and Monetary Affairs, Federal Effort Against Organized Crime: Report of Agency Operations, committee print, 90th Cong., 2nd sess., (Washington DC: June 1968), cited in Kristin M. Finklea, Organized Crime in the United States: Trends and Issues for Congress, Congressional Research Service (Washington DC: December 22, 2010), 4.

- Nelson D. Schwartz, “Branch Closings Tilt Toward Poor Areas,” New York Times, February 22, 2011, http://www.nytimes.com/2011/02/23/ business/23banks.html?pagewanted=all.

To speak with a scholar or learn more on this topic, visit our contact page.