- | Housing Housing

- | Research Papers Research Papers

- |

A Primer on State and Local Tax Policy: Trade-Offs among Tax Instruments

The primer begins with a short discussion of criteria for evaluating tax revenue options (i.e., economic efficiency, equity, transparency, collectability, and revenue production). It proceeds to an overview of the different types of taxes employed at various levels of government and an evaluation of each tax against these criteria. The tax categories included here are individual income taxes, consumption taxes, real property taxes, and corporate income taxes.

The choice of tax instruments by a state or local government has wide-ranging implications for the economy, and the amount of revenue to be raised should not be the sole criterion used in developing tax policy. The trade-offs between various tax instruments, including revenue, fairness, and collection cost, should all be incorporated in these decisions.

In a new study for the Mercatus Center at George Mason University, Justin M. Ross defines five criteria for evaluating tax policy and uses them to give a clear overview of the different types of taxes utilized by state and local governments.

Key Points

• There is no single type of tax that is unambiguously superior when it is evaluated in terms of revenue collected, collection costs, fairness, transparency, and minimizing distortions to the economy.

• These tax policy criteria often conflict with one another, and policymakers should consider trade-offs when deciding among the various policy choices.

• Every tax instrument can be made worse through poor design.

Tax Policy Evaluation Criteria

The following five criteria are widely used to evaluate tax policy. They are often in conflict with each other, and policymakers ultimately have to determine appropriate trade-offs.

• Economic efficiency. The imposition of many forms of taxes can result in individuals and businesses changing their behavior. For example, selective sales taxes can affect consumers’ choices about what to buy and where to buy it. Such changes in behavior, driven by tax policy, make society worse off by forcing people to make choices they would not have otherwise made. Tax policy should try to minimize such distortions in decisions.

• Equity. Equity, or fairness, can be thought of as occurring in two dimensions: (1) Horizontal equity means that two taxpayers who are in essentially similar situations pay the same amount of tax—for example, two people pay the exact same sales tax. (2) Vertical equity exists when an individual’s average tax rate remains constant as a share of income. Equity can be in conflict with other objectives, such as revenue production and collectability.

• Transparency. A tax should clearly define how it is calculated, and taxpayers should be able to predict the tax implications of any choice they make. Transparency generally declines as the complexities of a tax increase with regard to what is and is not taxable. For example, a tax becomes less transparent when differences in how income is received can affect the tax bill.

• Collectability. Any tax system imposes costs on those responsible for collecting the tax, whether they are government officials or vendors and employers. Income taxes that require taxpayers to be active in supplying information impose costs that are just as relevant as state and local tax department costs.

• Revenue production. Policymakers should always consider the significant costs that are generally incurred while raising revenue when they seek to determine whether the revenue potential of a tax justifies the undertaking. The revenue potential depends on both the size of the base to be taxed and the socially acceptable tax rate. Taxes that are frequently targeted by policymakers in the form of base narrowing or excessive rate increases can diminish productivity.

Tax Policy Instruments

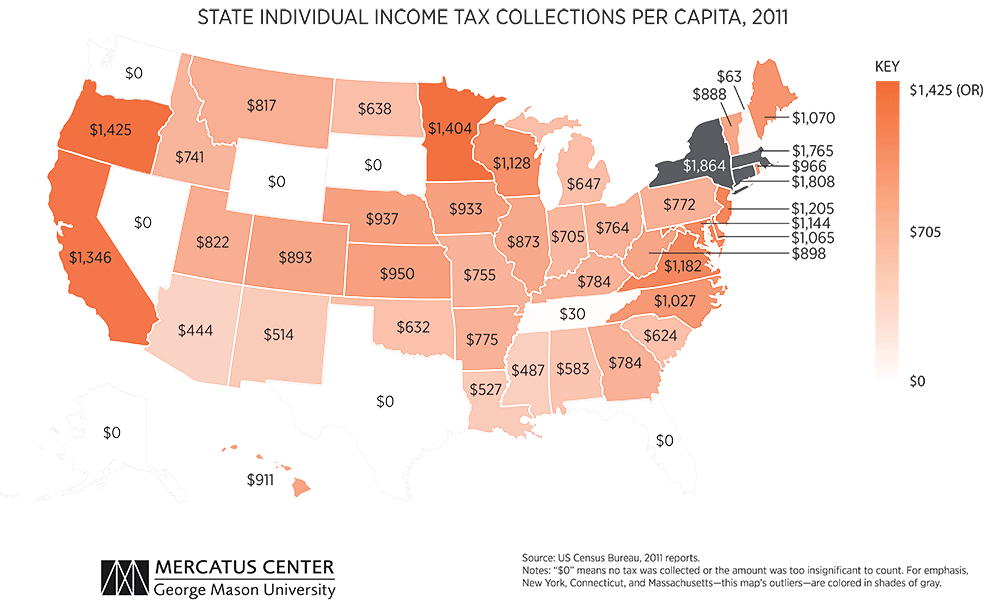

Individual Income Taxes

Forty-one states have some form of income tax, usually based on the federal income tax code. In many states, some types of local governments are also permitted to levy income taxes. Some key considerations follow:

• Limiting the definition of income or raising the tax rate makes an income tax less efficient, especially since workers can move between jurisdictions.

• Most income taxes are progressive, but states seem to have limited ability to engage in progressive taxation to reduce income inequality. Deductions and exclusions usually reduce horizontal equity.

• Similarity to the federal income tax model greatly reduces enforcement costs at the state and local level, so collectability is generally high, with some exceptions for the selfemployed and the wealthy with multiple residences.

• At rates that the states have historically levied income taxes, broad rate increases have typically increased revenue. This is less true in the case of more targeted income taxes directed at groups whose members can move relatively easily to escape the tax.

Consumption Taxes

Consumption taxes are levied against spending on household goods and services.

• With respect to efficiency, consumption taxes are favored as an alternative to income taxes by those wary of tax systems that punish savings.

• Consumption taxes are generally considered regressive, although consumption is arguably a better indicator of ability to pay among individuals with the same amount of annual income. Regressivity can also be modified by selective exemptions. Transparency falls as the number and complexity of exemptions increases.

• The burden of collectability falls mainly on the vendor. For out-of-state purchases, it falls on the buyer, who often does not report it.

• Revenues tend to be stable over time.

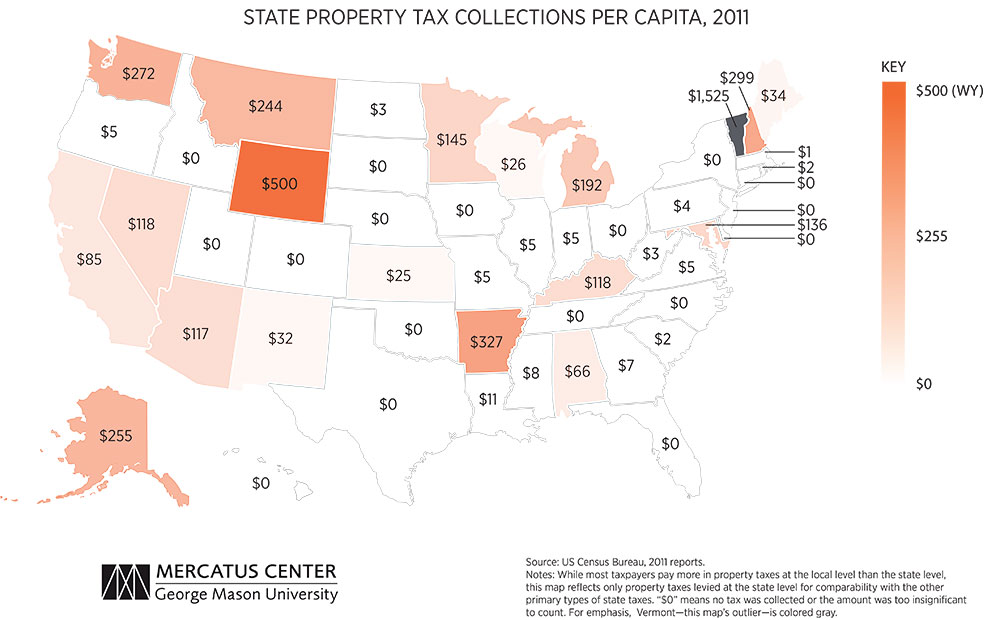

Real Property Taxes

Property taxes are assessed mainly at the local level. Localities determine how much they need to raise, and assess the value of all the taxable property in their jurisdictions. This determines the general tax rate and the tax level for each property.

• Real property taxes may be highly distortive since they tax business inputs.

• The equity of the tax depends on the accuracy of the property value estimates.

• Collectability is seldom a problem because the government is able to seize the property if the owner is delinquent.

• Property taxes are highly stable and serve as the primary source of local revenue. However, some states impose limits on the ability to raise property taxes.

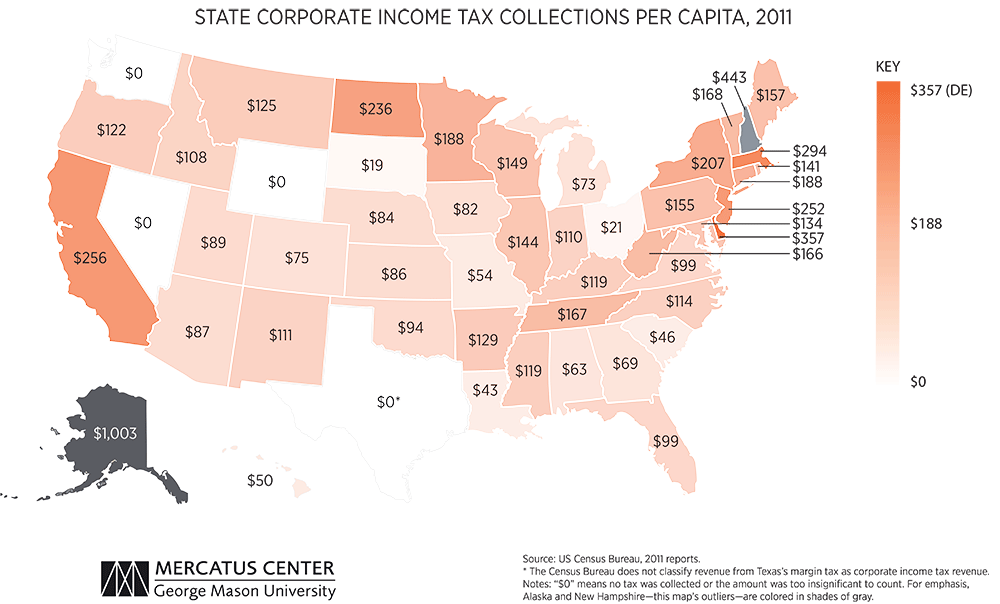

Corporate Taxes

Only four states do not tax corporate income. Most state systems have one rate and are based on the federal tax model.

• These systems impose large efficiency losses. They are a tax on capital, expose profits to double taxation, and dissuade small businesses from incorporating. They also encourage companies to issue debt rather than stock when raising capital.

• The vertical equity of a corporate income tax depends on how much of the tax is passed on to a company’s workers and customers.

State and local governments differ widely in both the amount of revenue they raise and the means by which they raise it. In “A Primer on State and Local Tax Policy: Trade-Offs among Tax Instruments,” Justin M. Ross describes four general tax systems commonly used by state and local governments. He evaluates them by the five criteria economists use for tax systems: economic efficiency, equity, transparency, collectability, and revenue production. The maps below show the average dollar amounts an individual pays for four commonly collected taxes throughout the 50 states.

Related Content

- | Housing Housing

- | Working Papers Working Papers

State Economic Prosperity and Taxation

- | Academic & Student Programs Academic & Student Programs

- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

The Deduction of State and Local Taxes from Federal Income Taxes

- | Housing Housing

- | Working Papers Working Papers

State Fiscal Condition: Ranking the 50 States | 2014 Edition

- | Government Spending Government Spending

- | Books Books

Freedom in the 50 States, 2013 Edition