- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

Would Taxing Banks Really Make the Banking System Safer?

In the wake of the 2007–09 banking crisis, some economists recommended imposing new taxes on banks. These proponents contend that policy makers could apply the taxes to correct “negative externalities,” or adverse spillover effects onto overall welfare, allegedly created by individual banks. Spillovers are assumed to arise from individually optimal bank decisions that fail to account for the higher risks that the aggregation of those choices might create for the banking system as a whole. Taxing banks is supposed to nudge the banks to restrain operations that contribute to total societal risks.

In the wake of the 2007–09 banking crisis, some economists recommended imposing new taxes on banks. These proponents contend that policy makers could apply the taxes to correct “negative externalities,” or adverse spillover effects onto overall welfare, allegedly created by individual banks. Spillovers are assumed to arise from individually optimal bank decisions that fail to account for the higher risks that the aggregation of those choices might create for the banking system as a whole. Taxing banks is supposed to nudge the banks to restrain operations that contribute to total societal risks.

It is unfortunate that these bank tax proposals fail to consider the unintended side effects of such taxes on the compositions of banks’ assets and liabilities. Even if taxes succeeded in inducing banks to restrain truly spillover-contributing operations, the resulting reshufflings of assets and liabilities would likely yield a riskier post-tax aggregate level of bank lending. Specifically, banks that already had been expending resources to screen and monitor loans would have strong incentives to respond to the tax either by cutting back on the high-quality loans that they had been making or by reducing their expenses by subjecting loans that they continue to make to less screening and monitoring. Such responses would undermine the intended benefits of imposing these taxes.

ALLEGED BANKING EXTERNALITIES AND HOW TAXES MIGHT CORRECT THEM

Allegedly, banking externalities can arise either in bank liability markets, such as markets for deposits or interbank borrowings, or in bank asset markets, such as markets for loans or securities. For instance, some economists have argued that spillovers in interbank borrowing markets can occur when any given bank that extends a loan to another institution takes into account only the risks of repayment delays or defaults on the part of that single institution. The borrowing institution could, in turn, use the funds to extend higher-interest loans to other institutions that make even riskier loans. Thus, the loan from the original bank could contribute to greater overall risks than that bank takes into consideration. Proponents of bank taxes suggest that apply- ing an appropriately calibrated tax rate to all interbank borrowings would induce banks to lend the socially optimal amount, thereby eliminating the potential for excessive borrowing across the banking system.[1]

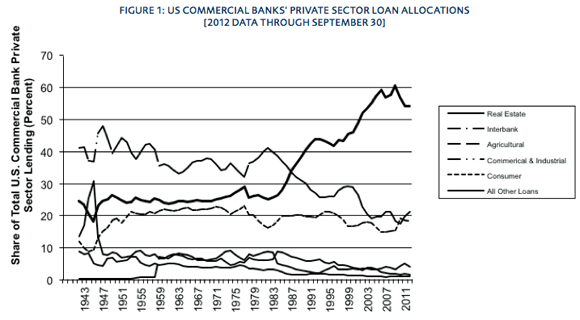

Tax proponents further contend that banks extend too many private sector loans, pointing to the upsurge in real estate lending between 1982 and 2006, shown in Figure 1. They say that this upsurge resulted in part from the failures of individual banks to recognize that as each bank boosted its real-estate lending, the resulting rise in aggregate lending reduced the pool of residual borrowers who were creditworthy. As all banks sought higher profits from boosting real estate lending, the pool of creditworthy borrowers was dissipated, which broadened exposure of the banking system to loan losses. Imposing an appropriate uniform tax rate on each additional dollar of real-estate credit, tax proponents suggest, would have nudged banks to reduce their overall lending and thereby prevented aggregate overlending from occurring.[2]

AN OVERLOOKED COMPLICATION: ALTERED ASSET AND LIABILITY COMPOSITIONS

Analysis of the logic of bank tax proposals reveals a complication that its proponents overlook: unintended adverse effects on banks’ efforts to contain loan losses.[3] Roughly half of a typical bank’s operating costs arise from expenses on labor and capital. For banks that take seriously efforts to restrain exposures to loan losses, significant portions of labor and capital resources are dedicated to screening loan applicants to determine which are creditworthy and to monitoring borrowers in an effort to prevent unproductive squandering of loan proceeds. Furthermore, as banks add labor and other variable inputs to fixed factors, such as equipment and facilities to screen and monitor additional lending, their per-unit expenses tend to rise. Just as any other firm seeking to produce a high-quality product faces increasing marginal cost of producing additional units, a bank’s marginal cost of screening and monitoring increases with its volume of lending. Consequently, as banks expand their lending, the additional expenses entailed to screen and monitor loans tend to increase more than proportionately. This fact automatically tends to limit the optimal scale of lending by cautious banks.

Of course, owners and managers at some banks may alternatively choose to direct spending to other purposes, including more plush office environments, executive perks, or other expenses unrelated to reducing risks of loan losses. Expanding lending generates additional revenues to banks to fund such expenses. Consequently, these banks are likely to be key contributors to any aggregate overlending problem that might exist.

Proposals to rein in potential bank overlending call for imposition of a single per-dollar tax rate on all bank credit extensions. Such a tax would fall equally on both banks that make good-faith efforts to contain exposures to loan losses and banks that do not. Of course, a uniform tax on loans would give both groups of banks incentives to reduce their lending, consistent with a pol- icy aim to prevent the overlending that drives up risks of loan losses. Banks that devote few resources to averting loan losses would cut back on credit extensions, thereby reducing their loss exposures as intended.

Now consider the effects of applying a uniform tax rate to the lending of banks that already allocate substantial resources to limiting loan-loss exposures. The immediate effect of the imposition of the tax on these banks would be to further ratchet up their expenses at initial scales of lending operations. There are two ways that these banks could opt to respond to the resulting higher lending costs. One reaction would be to extend less credit. On the one hand, this response is consistent with the aim of the tax, because pressures on the size of the pool of creditworthy borrowers are reduced when these loss-limiting banks cut back on their lending. On the other hand, lending cuts by these banks would yield fewer loans that otherwise would have been screened and monitored. Thus, higher-quality, lower-risk loans that these loss-limiting banks previously would have extended would not be made once the tax is imposed. Furthermore, banks that screen and monitor already incur the additional costs of performing these functions, which other banks choose not to incur, so imposing a tax expands the screening and monitoring banks’ already proportionately greater burden. Hence, these banks would more heavily feel the weight of the tax, which would induce them to reduce their lending by a proportionately larger amount than banks that made no special effort to limit loan losses.

An alternative response to the tax by the loss-limiting banks would be to cut back on expenses on existing lending operations in an effort to keep the scale of those operations close to the pre-tax level. Toward this end, the loss-limiting banks could reduce their employment of labor and capital resources, including some of the resources previously devoted to the screening and monitoring activities that normally would help con- strain their exposures to loan losses. These banks would have considerable incentive to contemplate responding in this way, given the resulting more-than-proportionate cost reductions that would help offset their new tax expense. Post-tax cutbacks in loss-limiting expenses by banks that previously had employed just-sufficient quantities of resources to the task of reducing risk exposures would cause them to become more heavily exposed to loan losses. They essentially would become more like the other banks that already had done little to avert risks of loan losses.

To sum up, one consequence of imposing a tax on bank lending would be an aggregate lending reduction consistent with the goal of combatting a perceived over- lending problem; however, another consequence would be an altered composition of aggregate lending. Banks that incur costs required to limit loan losses may reduce their lending by a larger amount than banks that forgo such expenses, so a smaller share of total post-tax lending would be screened and monitored as effectively as before imposition of the tax. In addition, some loss-limiting banks would engage in risk-reducing efforts less intensively than they did before the tax, and at least a few likely would opt to halt such efforts. On net, imposing the tax would simultaneously yield fewer total loans to be exposed to loan losses while having the unintended effect of leaving fewer loans remaining that banks would try to shield from such losses.

What about the effects of taxes intended to induce reductions in potentially excessive interbank borrowings? Realistically, a bank’s asset and liability allocations are interdependent; when the bank alters its liabilities, it usually reconfigures its assets. Imposing a tax on inter-bank borrowings thereby would give banks an incentive not only to contract those borrowings but also to reduce their lending—resulting in effects on aggregate credit quality analogous to those discussed above in regard to a tax on lending. In addition, banks would alter the post- tax composition of their liabilities in ways that conceivably could be riskier on net. Consider, for instance a tax on borrowing in wholesale interbank markets, much like a tax recently imposed on many banks in the United Kingdom. In the face of such a tax, banks could seek to cut overall expenses on other liabilities by substituting lower-expense subordinated debts for higher-expense equity capital that arguably provides a stronger buffer against losses to taxpayers in the event of a bank failure.

BETTER WAYS TO LIMIT “OVERLENDING” AND “EXCESSIVE” INTERBANK BORROWING

As is often the case with most actual and proposed government interventions, the imposition of bank taxes would have unintended effects. These effects generally would work against the overarching aim of increasing the safety and soundness of the US banking system.

While the upsurge in real-estate lending between 1982 and 2006 depicted in Figure 1 arguably involved some “excessive” interbank borrowings to support “overlending” in this bank loan category, it is far more likely that factors other than naturally occurring banking externalities caused these outcomes. These other factors include explicit and implicit government subsidies to borrowers and lenders in real-estate loan markets, capital regulations that provided banks with strong incentives to originate real-estate loans to sell to taxpayer-subsidized government-sponsored entities, and a Federal Reserve policy stance that artificially depresses the price of credit. Removing these contributors to “overlending” and “excessive” interbank borrowings would be much more effective at improving overall bank safety and soundness than imposing bank taxes, which could actually undermine this overarching public policy goal.

Footnotes:

1. For general overviews of bank taxation aimed at improving overall safety and soundness of the financial system, see Gianni De Nicolò, Giovanni Favara, and Lev Ratnovski, “Externalities and Macropru- dential Policy,” IMF Staff Discussion Notes, SDN/12/05, Interna- tional Monetary Fund, June 7, 2012; International Monetary Fund Staff, “A Fair and Substantial Contribution by the Financial Sector: A Final Report for the G20,” June 2010; Michael Keen, “The Taxation and Regulation of Financial Institutions,” NYU School of Law Collo- quium on Tax Policy and Public Finance, 2011; Ben Lockwood, “How Should Financial Intermediation Services Be Taxed?” Oxford University Centre for Business Taxation Working Paper WP 10/14, October 23, 2011; and Douglas Shackelford, Daniel Saviro, and Joel Slemrod, “Taxation and the Financial Sector,” National Tax Journal 63 (2010): 781-806. Discussion of taxes aimed specifically at curbing alleged “excessive” interbank borrowing include Viral Acharya, Lasse Ped- ersen, Thomas Philippon, and Matthew Richardson, “Taxing Sys- temic Risk,” in Regulating Wall Street: The Dodd-Frank Act and the New Architecture of Global Finance, eds. Viral Acharya and Mat- thew Ricardson, New York University (New York, 2011) 121-142; Enrico Perotti and Javier Suarez, “A Pigouvian Approach to Liquid- ity Regulations,” De Nederlandsche Bank Working Paper No. 291, April 2011; and Hyun Song Shin, “Macroprudential Policies Beyond Basel III,” Policy Memo, Princeton University, November 22, 2010.

2. Examples of proposals to tax alleged bank overlending (or con- sumer overborrowing) include Javier Bianchi, Emine Boz, and Enrique Mendoza, “Macroprudential Policy in a Neo-Fischerian Model of Financial Innovation,” (unpublished manuscript, Decem- ber 2011) University of Wisconsin and New York University, Inter- national Monetary Fund, and University of Maryland; Javier Bianchi and Enrique Mendoza, “Overborrowing, Financial Crises, and ‘Macroprudential’ Policy,” International Monetary Fund Working Paper WP/11/24, February 2011; and Olivier Jeanne and Anton Korinek, “Managing Credit Booms and Busts: A Pigouvian Taxation Approach,” Peterson Institute for International Economics Working Paper WP 10-12, September 2010.

3. See Enzo Dia and David VanHoose, “Using Pigouvian Taxes to Cor- rect Banking Externalities: A Cautionary Tale,” (unpublished manu- script, November 26, 2012) Università degli Studi di Milano-Bicocca and Baylor University.