- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

Introduction: A Principled Approach to Tax Expenditures

A roadmap for a more efficient, fair, and growth-oriented tax code

Introduction

The US tax code is riddled with tax expenditures—special deductions, credits, and exclusions that reduce taxable income for individuals and businesses. While some of these provisions serve a legitimate purpose—such as limiting the double taxation of income—many tax expenditures distort economic decision-making, create unfair advantages, and complicate the tax system. They also reduce revenue to the benefit of special interests while requiring tax rates to be higher than they would otherwise be.

Tax expenditures exist because of how the tax base is defined—that is, the income or economic activity chosen to be taxed in the first place. The larger moral issue with the current US tax code and its myriad of tax expenditures is that, as economist David Bradford once wrote, “Although the federal tax system by and large relates tax burdens to individual ability to pay, the tax code does not reflect any consistent philosophy about the objectives of the system.”

Since the 1970s, however, there has been a great deal of effort to come up with alternatives to the current system. One such alternative is the flat tax model. This model defines the tax base more narrowly, typically focusing on consumption rather than all income, with a single tax rate and few deductions. Another alternative system is the cash flow tax model, which focuses on actual cash flows, taxing all inflows while making investments immediately deductible, effectively creating a consumption tax that encourages saving and investment while maintaining progressivity. Yet, another system is the comprehensive income tax base, which seeks to tax all forms of income—whether from wages, investments, capital gains, or business profits—under a single, broad-based system. The comprehensive income tax model aims to eliminate tax preferences and loopholes, treating all sources of income equally to maximize fairness and efficiency.

The current US system is a hybrid of the last two examples. The US tax system is primarily an income-based system, but it incorporates elements that push it partially toward a consumption-based approach. It is not a pure version of either model. On the income side, the current system taxes wages, salaries, business profits, interest, dividends, and realized capital gains following income tax principles. This penalizes savings and investments as many scholars have shown.

To compensate for punishing savings and investment, this system also has significant consumption tax features. For example, tax-advantaged retirement accounts (401(k)s, IRAs) allow income to be saved without immediate taxation; unrealized capital gains are not taxed until sold (deferring taxation); step-up basis at death can eliminate capital gains taxation entirely; and mortgage interest deductions and other housing incentives favor certain forms of consumption. So rather than a pure income tax (which would tax all increases in economic power) or a pure consumption tax (which would only tax what is consumed), the US system sits somewhere in between, creating a complex hybrid that reflects various political compromises and policy priorities over time, while making the tax code more susceptible to rent-seeking behavior.

How the tax base is defined fundamentally shapes discussions about what constitutes a "tax expenditure" versus "normal taxation." For example, whether the mortgage interest deduction is a special benefit or just part of the normal tax structure depends entirely on which tax base model is the starting point. Different models also create different incentives around work, saving, investment, and consumption, with profound economic effects over time.

With that in mind, this report attempts to provide some clarity about which tax expenditures would exist or be terminated depending on how the tax base is defined. It begins by outlining a framework for broadening the base--identifying provisions under current law and proposing reforms to make the tax code neutral, simpler, and fairer.

We take the position that the Hall–Rabushka flat tax is the ideal system. Adopting that system would make this exercise about what tax expenditures should be retained or discarded very simple. The tax base determines what is and what is not a tax expenditure. By design, the tax base excludes several items. Then we look at which tax expenditures would be preserved.

While the Hall--Rabushka system provides a clear benchmark, our current tax code represents a significant departure from it. In an attempt to move toward a more neutral and consumption tax base while contending with political realities, we examine the many existing tax expenditures and classified them into three broad buckets:

- Tax Expenditures to Retain: Provisions that are essential to accurately measure income, prevent double taxation, or serve broad public purposes without introducing undue complexity.

- Tax Expenditures to Eliminate: Provisions that create unjustified preferences, distort economic decisions, or act as government subsidies for particular industries or groups. Their removal would broaden the tax base, enabling lower overall rates.

- Tax Expenditures We Would Rather Repeal but May Simply Have to Reform: Provisions to be reformed and restructured for neutrality, efficiency, or fairness if they can’t be eliminated.

In doing so, this report provides a roadmap for a more efficient, fair, and growth-oriented tax code. It also offers a long list of pay-fors for legislators interested in consolidating the nation's dire fiscal finances.

Section 1

1. The Ideal Tax Base: The Hall-Rabushka Flat Tax

The Hall–Rabushka flat tax is a single-rate consumption tax that removes taxes on savings and investment income, effectively turning it into a consumption-based system. It eliminates most deductions, credits, and loopholes while taxing all income at a uniform rate. The system consists of two main components: an individual wage tax and a business tax.

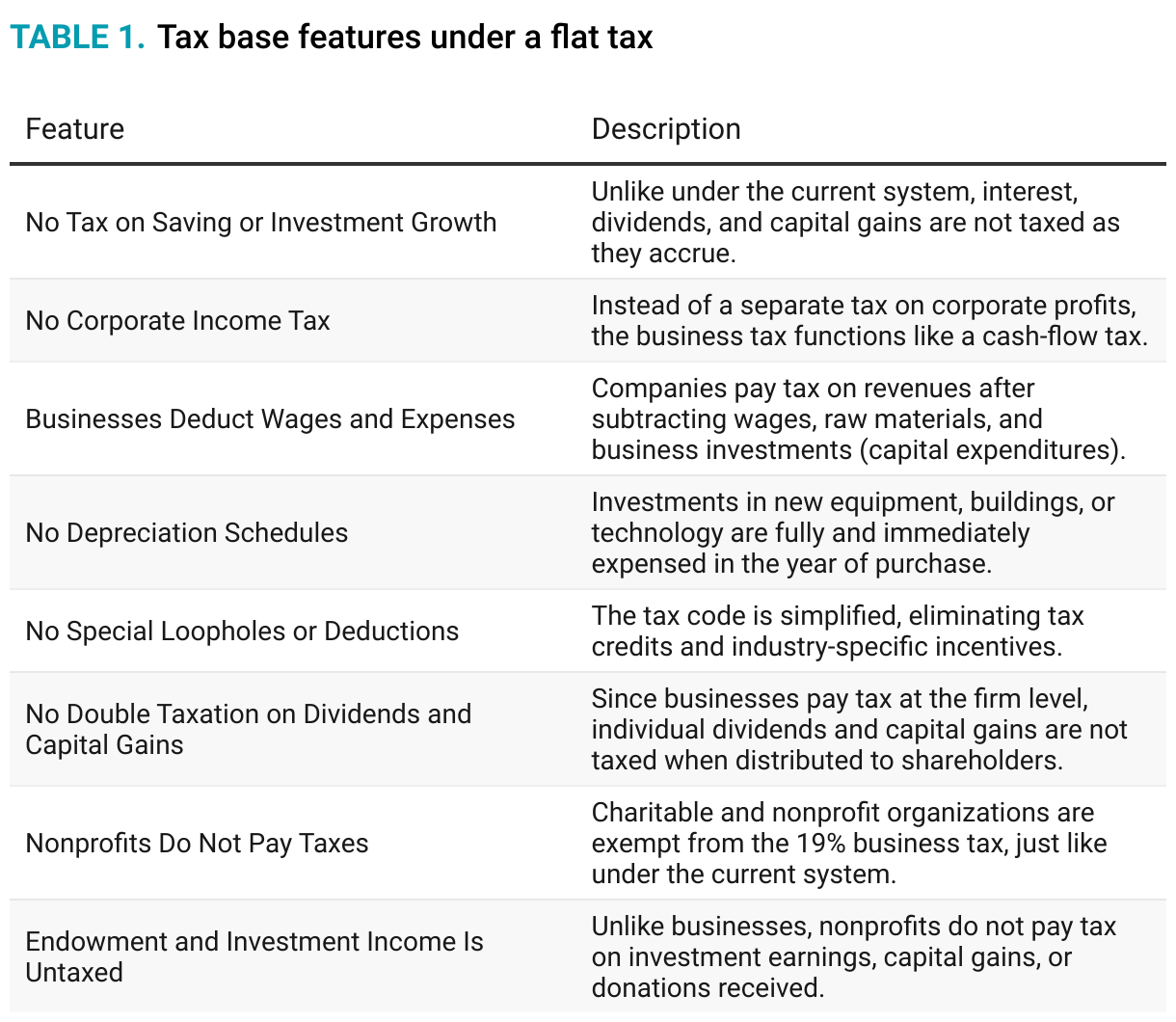

Under the individual wage tax, individuals pay a flat 19% tax on wages, salaries, and pension benefits but only on income above a generous personal allowance (e.g., $25,500 for a family of four). For instance, an individual earning $100,000 who chooses to save $50,000 and spend the remaining $50,000 would only be taxed on their consumed income after applying the personal exemption. If the taxpayer is a married filer with two children, they receive a $25,500 exemption, reducing their taxable consumption to $50,000 ﹣ $25,500 = $24,500. This amount is then taxed at the flat rate of 19%, resulting in a tax liability of $4,655. The $50,000 saved is exempt from immediate taxation and grows tax free. In the future, when these savings are withdrawn and spent, they will be taxed at 19%, ensuring that income is taxed only once—at the point of consumption. This tax model would eliminate the need for 401(k)s, Roth IRAs, and other tax-advantaged retirement accounts because it inherently treats all savings as if they are held in tax-deferred accounts. This structure encourages saving and investment while simplifying the tax system by eliminating the need for deductions, credits, and complex tax rules. There are no deductions for mortgage interest, state taxes, charitable donations, or other expenses. Additionally, investment income—such as interest, dividends, and capital gains—is not taxed at the individual level.

The business tax applies a flat 19% tax on net business cash flow, meaning businesses deduct wages and material costs but not interest payments (as to create a tax preference for debt over equity financing). Unlike under the current system, under Hall–Rabushka, businesses can immediately expense capital investments, eliminating the need for depreciation schedules. This is important because under depreciation rules, due to the time value of money, someone who makes a capital investment may never recover the full cost of their investment under depreciation schedules. This problem is further exacerbated during periods of high inflation.

The Hall–Rabushka tax also follows a territorial system, meaning US businesses are taxed only on their domestic profits, not on earnings made and taxed abroad.

The payroll taxes that fund Social Security would not change under a flat tax. This means that employees and employers would still pay payroll taxes, and these contributions would not be deductible against flat-tax wages. Since Social Security benefits are funded by already-taxed wages, taxing them again upon withdrawal would violate the principle of taxing income only once.

A key advantage of the flat tax is its simplicity—tax returns could fit on a postcard. It also ensures that every dollar of income is taxed once and only once, preventing double taxation on savings and investments. The system is growth oriented as it removes investment disincentives, thereby leading to higher economic productivity. Additionally, the broad tax base allows for a lower overall tax rate, making the system potentially revenue neutral if economic growth expands the tax base.

In summary, these are features of the tax base under a flat tax:

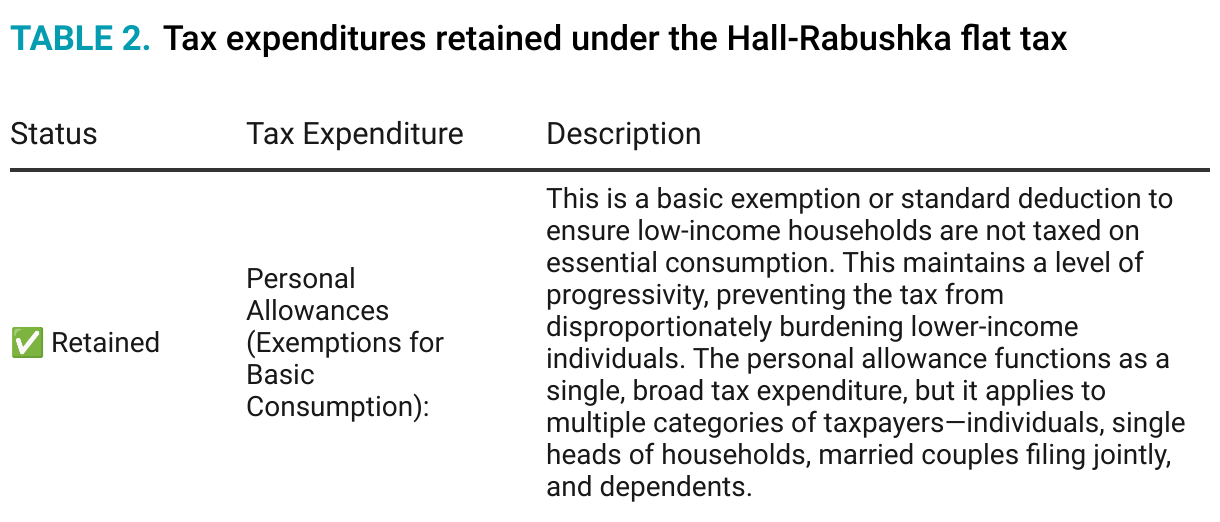

Here’s the tax expenditure that would remain under the Hall–Rabushka Flat Tax:

Although this provision could be technically broken down into different components (e.g., an allowance for each taxpayer vs. allowances for dependents), in policy terms, it is generally considered one unified tax expenditure because it serves the same function across all categories: shielding a base level of income from taxation to ensure progressivity in the otherwise flat-rate system.

There are several alternative versions of the flat tax, each with different approaches to tax expenditures. While the Hall–Rabushka Flat Tax is the most well known, other flat tax proposals keep the same tax base (hence share what is and what is not a tax expenditure) but allow a few additional tax expenditures. The Armey Flat Tax, named after Congressman Dick Armey, is based on the Hall–Rabushka model but includes some politically minded tax expenditures. In addition to the personal allowance, it retains deductions for charitable giving, provided donations are made to qualified nonprofit organizations. The Armey Flat Tax also allows for a transition period when mortgage interest deductions could remain. By keeping some popular deductions–such as for charities and homeownership–Armey’s version attempts to be more politically viable. The same is true of the Forbes Flat Tax, which also retains the charitable deduction to encourage philanthropy. The argument is also that such donations do not constitute personal consumption. The Forbes Flat Tax also retains the mortgage interest and adds a deduction for tuition and education expenses to support investment in human capital.

Section 2

The Current System: A Hybrid Income-Consumption Tax System

The current US federal tax system is a hybrid that combines elements of both income and consumption taxation. This structure has evolved from the traditional Haig–Simons income definition, defined income as the total of an individual's consumption plus the change in their net worth over a given period. This comprehensive measure aims to capture an individual's ability to pay taxes by considering both spending and savings. However, implementing a pure Haig–Simons income tax poses challenges, such as accurately measuring unrealized gains and accounting for non-cash benefits.

To address these challenges and various policy considerations, the US tax system has incorporated elements of consumption taxation:

- Retirement Accounts: Contributions to plans like 401(k)s and IRAs are tax deferred, meaning taxes are paid upon withdrawal during retirement. This approach encourages saving, by taxing income when it is consumed rather than when it is earned.

- Tax-Preferred Savings Accounts: Vehicles such as Health Savings Accounts (HSAs) and Education Savings Accounts allow for tax-free growth, provided the funds are used for specified consumption purposes.

- Consumption Taxes: While the federal government primarily relies on income taxes, it also imposes excise taxes on specific goods and services, functioning as consumption taxes. Additionally, state and local governments often levy sales taxes on goods and services.

The integration of income and consumption tax elements has led to several issues. The tax code has become increasingly intricate, with numerous deductions, credits, and exemptions. According to the Department of Treasury there are 170 tax expenditures. These expenditures carve the tax code, making the tax code remarkably burdensome and arbitrary for taxpayers. The convoluted nature of the tax system has also made it remarkably inefficient, resulting in increased compliance costs and resource allocation toward tax planning rather than productive economic activities. Such a system is also deeply unfair because it favors those with access to specialized tax advice and the ability to navigate or exploit complex provisions.

Transitioning to a flat tax or a cash-flow tax system may be challenging in the current political landscape. However, policymakers can still strive for a simpler tax system that is broader, fairer, and more neutral. This involves eliminating tax expenditures that serve as pure tax breaks for special interests, retaining those that prevent double taxation of income, and reforming others that, while ideally removable, are politically sensitive.

By focusing on these strategies, policymakers can work toward a tax system that is simpler, less distortive, and more conducive to economic prosperity.

The following a list of tax expenditures to retain under a hybrid tax system, along with the justification for each:

By retaining these tax expenditures, the tax system aims to prevent double taxation, promote savings and investment, and ensure fairness.

The following is a list of tax expenditures to replace with full and immediate expensing:

The following is a list of tax expenditures to repeal or reform:

The following is a list of tax expenditures to repeal, along with the justification for each:

Supporting documents